Table of Contents

Welcome to the Blockhead Business newsletter, your go-to source for industry developments, news and insights in the world of digital assets.

Asia-led and global in scope, we bring you a weekly roundup of the most important business and economic developments in the industry, along with expert analysis and commentary from top professionals in the field.

Whether you're a fund manager, professional investor, or simply interested in the world of digital assets, our newsletter is your essential guide to navigating the future of finance.

CAPITAL FLOWS IN GLOBAL MARKETS

Bitcoin Reigns Supreme in Q1

At the close of a volatile quarter in markets, optimism about expected rate reduction is driving animal spirits — and worry.

After a brief "crypto winter," Bitcoin, the notoriously volatile digital currency, again topped the scoreboard as the best-performing asset class by a wide margin in the first quarter.

Those trading moves happened despite increased regulatory scrutiny in the digital assets world.

Silicon Valley Bank (SVB) collapsed in early March due to massive losses on its bond portfolio as rates skyrocketed, warning markets that monetary tightening would certainly bring greater misery.

Still, Bitcoin closed the quarter with a gain of 72%, making it its best quarter since the three months ended in March 2021, when it soared by nearly 103%.

Compared to the S&P 500's 7% rise, the Nasdaq 100's 20.5% growth, and the iShares 20+ Year Treasury Bond ETF's 6.8% growth, the world's largest cryptocurrency clearly came out on top.

Stocks & Bonds at Risk

Despite those gains in equity markets, top investors have stopped pursuing the last stock boom because they believe the hopes for a more lenient monetary policy from the Federal Reserve are unfounded while inflation remains high.

Any rate reduction, in their view, would be made to arrest an economic slump that would also be bad news for market returns.

Two weeks after opening it, Barclays Wealth Management finally unwound its overweight position in developed market equities.

After deciding that the US economy would feel the impact of aggressive tightening for months to come, Legal & General, which oversees $1.4 trillion, reduced its stock position to its largest underweight since the epidemic.

Deutsche Bank AG reports that asset managers moved their equity exposure from near neutral to a level halfway towards historically low underweight measures after this month's banking upheaval.

The markets are focusing on dropping bond rates and optimistic readings of a looser Fed balance sheet to forget about fears of banking sector contagion.

One of the most volatile quarters in years has ended, yet Treasuries posted their greatest quarterly return since 2020.

The start of Japan's fiscal year, which might lead to stronger purchases by investors there, a weekly pause in note and bond auctions, and a recent surge in flows into US government bond funds are all factors that bode well for the bond market in the near term.

Yet, this doesn't mean the market will be unidirectional.

If the monthly US employment data scheduled to be released on Friday comes in higher than expected and rekindles anticipation for the Federal Reserve's extra interest rate rise in May, it might shock the market.

Given that it occurs during a trading session shorter than usual due to a vacation, its significance may be magnified.

Jobs Data to Drive Sentiment

Similarly to how a predicted slowing in pay growth may reassure Fed policymakers in their inflation war, the rate of hiring in the US in March likely continued to indicate solid though declining labour demand.

The consensus forecast from a Bloomberg survey of analysts is for non-farm payrolls to increase by over a quarter million in March, following an increase of 311,000 in February.

Over the past 11 months, the world's largest economy has seen employment growth beyond estimates. This is the longest such streak since Bloomberg began tracking this data in 1998.

The March jobs report will be the last before the Fed's meeting on May 2-3, when they will determine whether to continue raising the benchmark interest rate.

Central bankers are considering the cumulative effect on lending conditions of their rate-hiking campaign over the last year, although underlying inflationary pressures remain robust.

Before the recent demise of major banks, however, lending criteria were already stringent.

WHAT'S IN STORE?

Next week we will get US jobs figures. Markets remain nervous about the outlook for jobs, but this will take time to be reflected in payroll numbers.

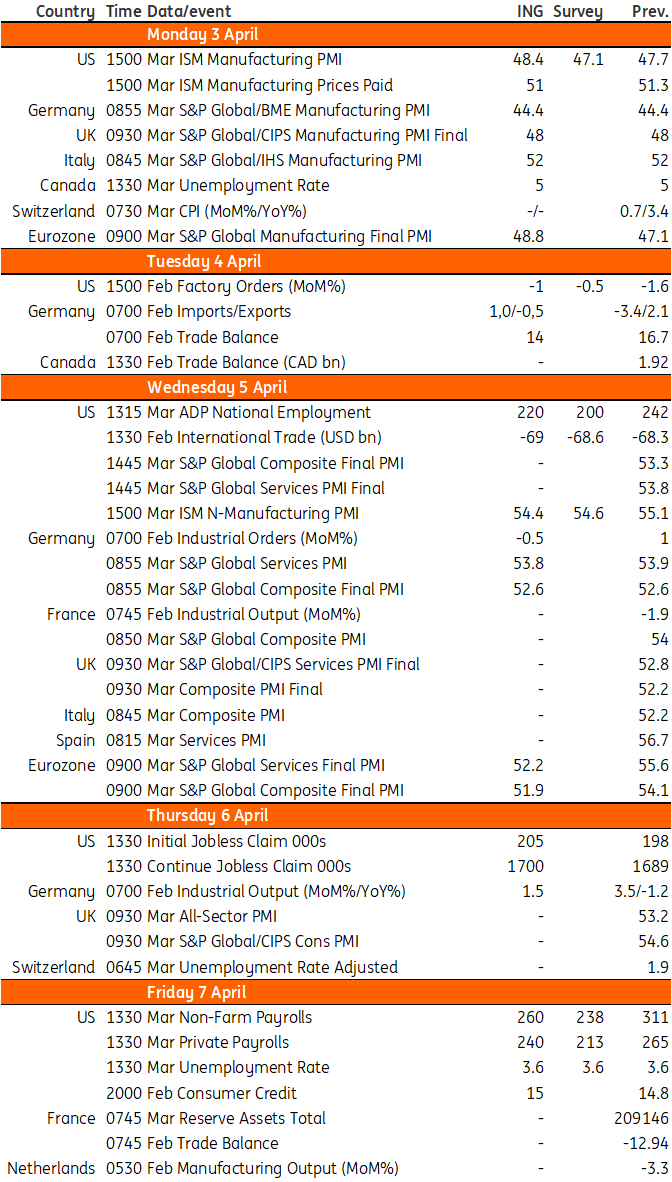

Macro Calendar: Key Events in Developed Markets

🇺🇸 United States: If There's a May Hike, it Will Be the Last

Whether the Fed will raise interest rates at its May 3rd Federal Open Market Committee (FOMC) meeting is still contentious in financial markets.

So far, officials have been hesitant to take any firm action, opting instead to gather more information on the potential impact of the current banking sector crisis on financial stability.

Friday, April 5th, will provide US employment data, and Thursday, April 12th, will bring US consumer price index data.

The tightening of lending conditions due to financial difficulties will be a huge headwind for struggling firms, causing the markets to remain anxious about the employment picture. However, this will take some time to show up in payroll data.

A rate hike of 25 basis points (bps) is widely expected if the increase in payrolls for March is over 200,000.

On the activity side, we will be keeping a close eye on car sales figures and ISM business surveys, and we will also be listening closely to the words of individual Fed officials.

Financial markets are pricing in a 25 bps rise on May 3rd, but they anticipate this will be the final increase in the policy rate. Markets were already worried about tighter lending standards, a weakening property market, and pessimism among America's top corporate executives.

The potential for failure for all three of them will increase if banks continue to experience difficulties.

This raises the possibility that inflation may fall more rapidly, allowing the Fed to respond with interest rate reduction before the end of the year as the danger of a harsh landing for the economy rises.

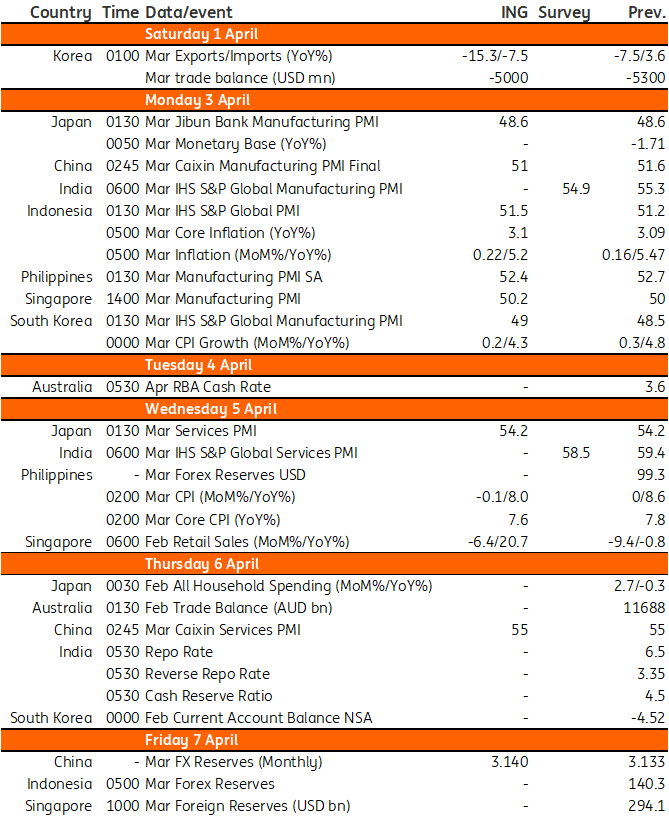

Asia Week Ahead: Policy Rate Decisions From Australia & India

Next week features policy rate decisions from Australia and India. Korea, Indonesia, and the Philippines will release inflation data, while China and Singapore will report on economic activity.

Macro Calendar: Key Events in Asia Next Week

🇦🇺 Australia: End of Rate Hikes?

Inflation in February was lower than predicted, so markets anticipate the Reserve Bank of Australia (RBA) will maintain its current cash rate goal of 3.6% when it meets next week.

These inflation data provide credence to the RBA's previous signal that it was considering a rate pause at its most recent rate-setting meeting. Current market pricing suggests that 3.6% is the ceiling.

🇮🇳 India: Inflationary Pressures Persist

With both headline and core inflation elevated, markets anticipate that the Reserve Bank of India will raise rates by 25 bps at its April meeting, bringing the repo rate to 6.75%.

As inflation is expected to decline dramatically in March, the markets believe this may be the final walk of this cycle.

🇰🇷 Korea: Trade & Inflation Data

China's reopening narrative has failed to help Korea's exports, and March trade statistics will show that global demand for semiconductors could be more active.

According to the markets, the trade gap is expected to reduce in March due to a steep drop in imports rather than a rise in exports.

Meanwhile, March should see a further deceleration in consumer price inflation. The decline in oil prices should more than counteract the rise in food and utility costs.

The markets have long predicted that the Bank of Korea (BoK) is finished hiking for this cycle because the CPI is expected to climb to 3% in the next months.

🇨🇳 China: Diverging Pace of Recovery in Manufacturing & Services

Caixin's manufacturing PMI is expected to show weaker monthly growth than the official PMI survey since its respondents tend to be smaller enterprises.

This is because small exporters are the first to feel the effects of a slowing US and European economies.

Caixin services PMI respondents, on the other hand, should benefit more from retail sales growth than official PMI survey respondents, who are more likely to be involved in the real estate industry.

China's foreign currency reserves to shed light on money circulation.

On April 7th, China will reveal its March foreign exchange reserves. Since the United States and Europe are at the centre of the financial market upheaval, this information is crucial for determining the course of cross-border capital flows.

Because of its distance from the epicentres of the turbulence and its improving economy, China is expected to see a modest influx in March.

🇸🇬 Singapore: Retail Sales to Rebound

Using last year's numbers as a reference point, February retail sales in Singapore might rise by 20.7%. Yet, as higher inflation maintains a lid on economic activity, sales are expected to fall from the previous month.

A lacklustre GDP result for the first quarter can be expected due to sluggish retail sales, a decline in industrial production, and a drop in non-oil domestic exports.

🇮🇩 Indonesia: Inflation Data

While core inflation is expected to remain stable at 3.1%, headline inflation in Indonesia may decline to 5.2% annually (from 5.5% earlier).

Bank Indonesia Governor Perry Warjiyo has left interest rates unchanged for two meetings because core inflation is extremely near the central bank's inflation objective of 3%.

🇵🇭 Philippines: Inflation Data

In the Philippines, annualised price increases are predicted to have fallen 8% from 8.6% in the previous month.

The Bangko Sentral ng Pilipinas may take a breather at their May policy meeting if inflation slows further in the Philippines.

If inflation continues downward, Governor Felipe Medalla may have raised interest rates for the last time in this cycle.

BLOCK BUSINESS INSIGHTS

Global Stress? Not For Bitcoin as it Reigns Supreme

Bitcoin's unexpectedly quick recovery from its "crypto winter" has again placed the famously volatile digital currency at the top of the leaderboard as the best-performing asset class by a wide margin in the first quarter.

China's Confusing Tunes on Crypto Regulation

China is officially worried about US banks' crypto exposure, but at the same time, Chinese banks working out how to support Hong Kong crypto firms.

In the era of digital finance, regulatory technologies and capabilities must be kept up to date to ensure financial innovations do not come at the cost of stability, said Xuan Changneng, deputy governor of PBOC, at the #BFA2023 today, Shanghai Securities News reported. pic.twitter.com/DmBsAQtnJI

— Yicai Global 第一财经 (@yicaichina) March 31, 2023

so, on the one hand, we have China officially worried about US banks' crypto exposure, and on the other, we have Chinese banks working out how to support Hong Kong crypto firms... not a conspiracy theorist, but it's almost like they're mocking now? https://t.co/rnVH3IqGiG

— Noelle Acheson (@NoelleInMadrid) March 31, 2023

US$1.6 Billion Pulled From Binance After US Watchdog's Bite

A US watchdog bit Binance and now investors are pulling money out of the exchange. After the CFTC lawsuit, investors pulled US$1.6 billion in cryptocurrencies from Binance, according to blockchain data tracker Nansen.

CFTC Sues, Says Compliance Efforts at Binance a Sham

The US has taken its strongest action against Binance Holdings and its chief executive officer, Changpeng Zhao, according to a court filing on Monday.

FEATURED & EDITORS' PICKS

We Passed Elevandi's Digital Assets Knowledge Certificate But It Wasn't Easy

Blockhead passed Elevandi's Digital Assets Knowledge Certificate with a score of 90%, but it's certainly not for everyone...

The CFTC's Binance Case as a Roadmap

An alternative reading of the charges is a map of how to run an offshore exchange that the US will not complain about.

BlockBeat: Coinbase, Do Kwon and Justin Sun vs. the World

Crypto villains and crypto exchanges alike are being hunted by US authorities, whilst zkEVM competition ramps up.

Blockhead Brief: Singapore Leads Crypto Layoffs

Singapore is the king of crypto layoffs, Arbitrum enters the Top 40, Fujitsu files a trademark, and an Amazon boo boo excites web3 bulls.

Despite a Dip in Confidence, Singaporeans Continue to Invest in Cryptocurrency

A new study by Independent Reserve shows that Singaporeans are still actively investing in digital assets, and outlines the attitudes of different segments of Singapore's population towards cryptocurrency.

INDUSTRY NEWS

BitKeep to Rebrand as Bitget Wallet, Strengthen Security

BitKeep has announced its 2023 roadmap, which plans to rebrand the DeFi wallet as Bitget Wallet, strengthen the overall security system and revamp the management team.

OKX Seeks to Become Key Player in Hong Kong's Virtual Asset Industry with Licensing Applications

The announcement that it is applying for a Hong Kong VASP license under new regulatory regime follows more than a year of preparation and organizational design by OKX.

BEYOND THE ARTICLES

VIDEO: Turning His $200K CryptoPunks NFT Into A Band?

From rap duo, to street-busking, to turning a CCTV break-in footage into an MTV, and spending $200K on a CryptoPunks— Jayefunk is the man behind Manifest; the world's first CryptoPunks NFT band.

The world of Web3 can be quite a whirlwind. Here at Blockhead, we understand how busy crypto is keeping you, so we send out three newsletters each week: BlockBeat for a wrap-up of the week’s news; Blockhead Brief for weekend happenings as well as what to look forward to in the week ahead; Business Bulletin for the most important business and economic developments in the industry. To avoid FOMO and access member-only features, click here to subscribe. Stay tuned, and have a lovely week ahead!

{kind=link}