Table of Contents

Prediction markets have had a remarkable year of mainstreaming. Combined volume on Polymarket and Kalshi reached $85 billion in the first four months of 2026. Robinhood reported that its own prediction market offering — event contracts — grew 320% year-over-year in Q1, becoming one of the fastest-growing revenue lines on its platform.

Washington is paying attention: three of the biggest ETF issuers — Roundhill Investments, GraniteShares, and Bitwise — filed with the SEC in February to launch products seeking to capitalise on booming interest in prediction markets. Those funds were supposed to begin trading this week. The SEC intervened before the deadline and asked for more information about how the products actually work.

It is a reasonable question. Because the picture that emerges from the underlying data is considerably less flattering than the social media narrative.

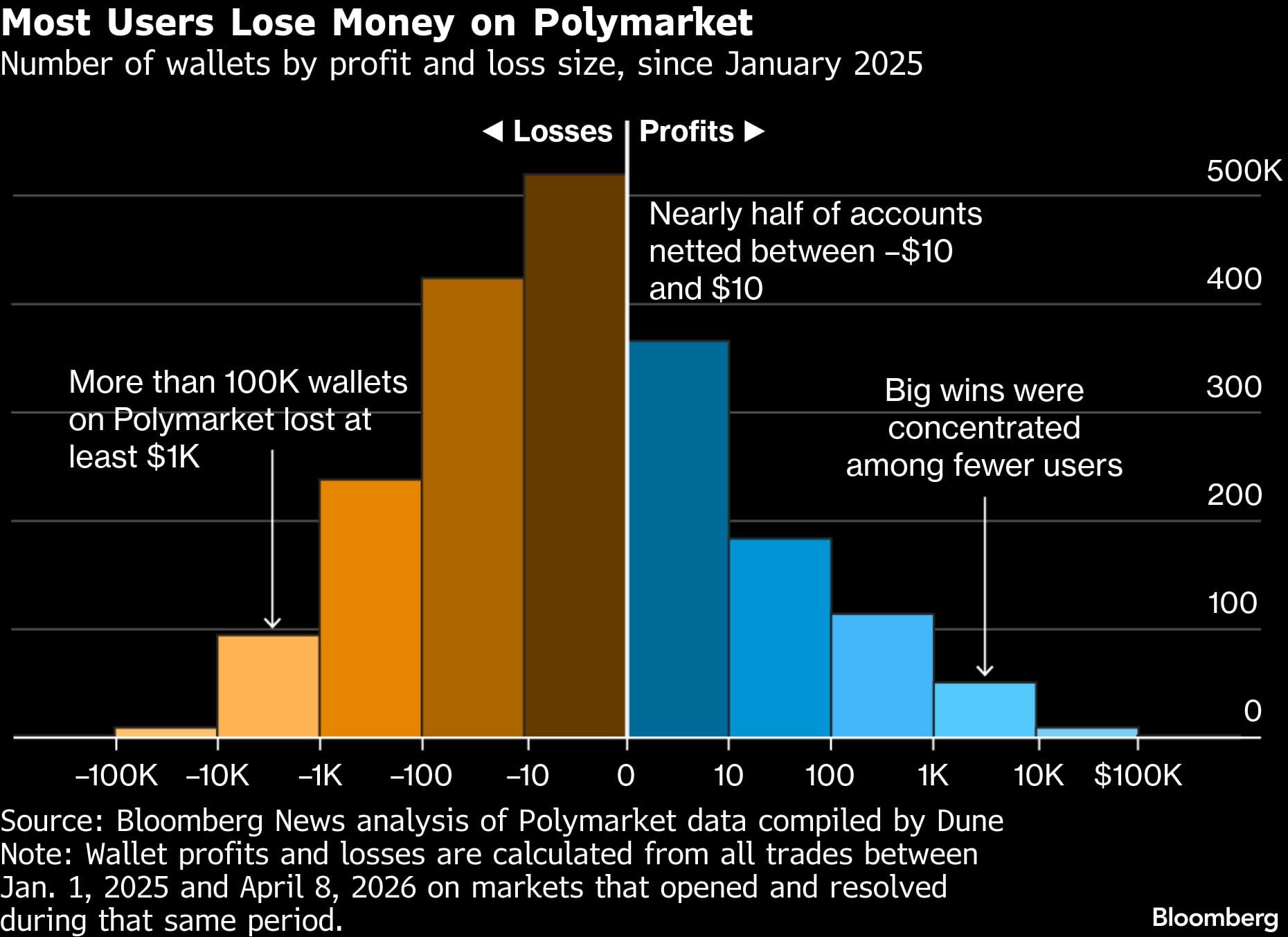

Prediction markets are being touted on social media as a lucrative side hustle for young Americans squeezed by rent and student loan bills. In reality, most traders are losing money, and a significant amount in many cases. Over 100,000 accounts lost at least $1,000 on Polymarket since the beginning of 2025 — almost twice the number that made at least that much, according to a Bloomberg News analysis of every wallet active since the beginning of 2025.

Among the winners, a majority of the profits were raked in by a tiny slice of what appear to be automated bots, based on Polymarket trade records compiled by data firm Dune. Everyone else, in aggregate, lost $131 million.

The bot advantage is not, it turns out, about being smarter. University of San Diego researcher Joshua Della Vedova found that retail traders actually picked the winning outcome more often than the automated accounts. They lost anyway, because they entered positions later and at worse prices. Automated accounts averaged 89 trades on each active trading day, compared to 2.2 for non-bots, spread across a greater diversity of markets. The edge was structural, not informational.

A detailed analysis by researcher Federico Glancszpigel, published last month on Medium, goes further in dismantling what he calls the "Polymarket Dream." Drawing on Della Vedova's study of 222 million trades, the core finding is as follows: traders with above-random forecasting accuracy earn negative returns on Polymarket — not zero, negative — because they arrive late to markets and pay unfavorable prices. Meanwhile, traders with near-random directional accuracy earn positive returns through execution quality alone.

The implication is that the forecasting model — the thing every AI-agent Twitter thread is selling — is largely irrelevant to realised profit at the margin. Automated traders achieve 2.52 cents of price improvement per contract relative to manual participants. Compounded across thousands of contracts, that structural edge is what separates the top of the return distribution from everyone else.

The data problems compound the picture. The study notes that 25% of Polymarket's historical trading volume is attributable to wash trading — accounts transacting with themselves to inflate activity metrics. In December 2024, this figure peaked at approximately 60%. Volume figures widely cited in financial media are effectively inflated by around 2x once both adjustments are applied.

None of this means prediction markets are illegitimate. The platforms are real, the volume is real, and a small number of players are extracting substantial profits. A French trader known as "Théo" deployed $85 million in the 2024 U.S. election markets and earned a profit of equivalent magnitude, verified on-chain. Cross-platform arbitrageurs have extracted an estimated $40 million in realised profit by exploiting price discrepancies between Polymarket and Kalshi. The top 1% of accounts capture 84% of aggregate trading gains. The market functions. It is just that it functions very well for a very small number of professional operators, and very poorly for most everyone else.

This is the context in which the SEC's delay of prediction market ETFs lands differently than it might otherwise. Unlike funds tied to Bitcoin or indices, prediction market ETFs are structured more like binary contracts, meaning investors could lose substantially all of their investment if a wagered outcome does not materialise. The proposed products would give retail investors exposure to these dynamics without requiring them to trade directly — which might sound like a feature, until you consider that the underlying market is one where, even when retail participants predict correctly, they tend to lose money.

The delay is expected to be temporary, according to people familiar with the matter. The ETFs will likely launch, and they will likely attract capital, because the narrative around prediction markets — democratised information, crowd wisdom, frictionless access to event-driven alpha — is a compelling one. The data suggests the reality is closer to a poker table where most players are funding the rake and a handful of professionals with faster cards.

{kind=link}