Table of Contents

There is a certain type of financial news that doesn't generate headlines but moves markets over years. No price surge, no celebrity. Just a press release about middleware. Broadridge's recent integration of Crypto.com into its NYFIX order routing network — enabling institutional brokers to route cryptocurrency orders through the same infrastructure they use for equities and fixed income — is that kind of news. Unremarkable on the surface. Telling in context.

Because the context is everything. This is not an isolated development. It is but one connection in a network of infrastructure, regulation, and institutional capital being methodically assembled around digital assets. The question of whether cryptocurrencies belong in institutional portfolios will not be answered through more debate because the infrastructure is already a reality.

The Plumbing Beneath the Market

FIX — the Financial Information eXchange protocol — has governed how trade orders move between financial institutions since 1992. It's the messaging standard that allows a fund in London to route an order to a broker in Tokyo without anyone picking up a phone. Standardised, auditable, and so deeply embedded in institutional operations that most major firms can't trade without it.

Crypto order routing can now run through the same system. That matters less as a headline and more as a symptom - that traditional finance is not building a parallel (and undoubtedly clunky) infrastructure for digital assets. It is extending its existing one.

Big Piece of a Bigger Puzzle

Broadridge-NYFIX sits within a clear and accelerating pattern. In April 2025, Ripple acquired prime broker Hidden Road for $1.25 billion — making it the first crypto company to own and operate a global, multi-asset prime broker, clearing $3 trillion annually and serving more than 300 institutional clients. That's not a crypto firm buying another crypto firm. That's crypto buying the pipes Wall Street runs on.

Kraken launched an institutional prime brokerage offering in mid-2025, providing access to liquidity across more than 20 global venues.

Commodity Futures Trading Commission (CFTC)-regulated derivatives exchange and clearinghouse Bitnomial launched a new U.S. clearing house for crypto derivatives, accepting digital asset collateral as margin for the first time — meaning institutions can post cryptocurrencies like Bitcoin or Ethereum without converting to cash.

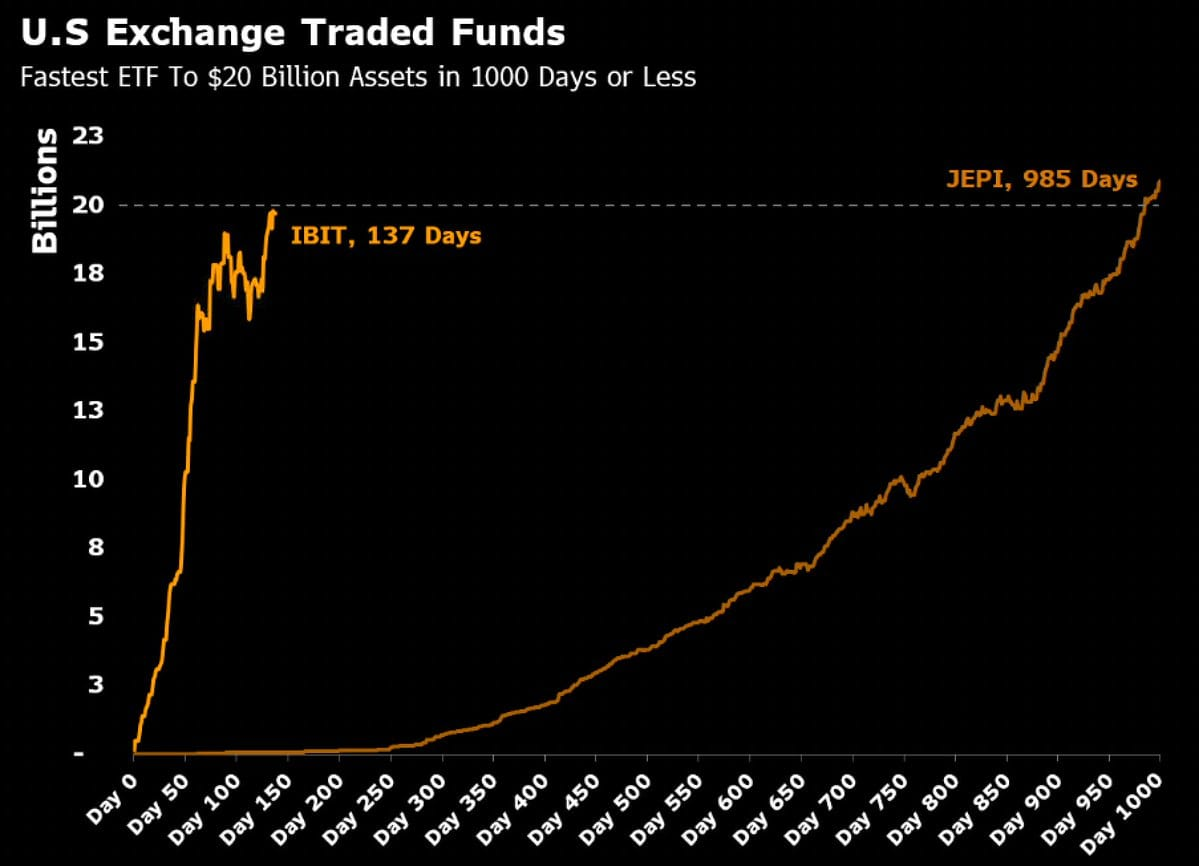

BlackRock's Bitcoin ETF (IBIT) became the fastest-growing in history. Public pension funds in Michigan and Wisconsin now list digital assets among long-horizon holdings.

Each of these is a data point. Together, they describe a market structure being built by people who have decided that the question of crypto's legitimacy is closed.

Knives to a Gunfight

The idea that institutional hesitancy around crypto was ideological — skeptical boards, Bitcoin-averse risk committees — was always a misdiagnosis. The actual blockers were operational.

Compliance teams couldn't map crypto transactions onto existing surveillance frameworks. Risk desks couldn't get standardised pricing feeds. Operations teams found that settling a crypto trade required entirely separate tools, logins, and reconciliation processes from everything else they did. In large financial institutions, workflow is no trivial consideration. It determines what is and isn't possible.

What the current wave of infrastructure buildouts are trying to do, collectively, is remove those blockers one by one. FIX connectivity. Institutional-grade custody. Prime brokerage. Crypto stops being a special case and becomes a line item.

A Ratchet, Not a Switch

Institutional adoption of a new asset class is never a single moment. Think about how hedge funds came to embrace derivatives in the 1980s and 1990s. No single event catalysed it — just a progressive accumulation of legal frameworks, accounting standards, risk models, and trained talent. Each institution that built a derivatives capability made it slightly more acceptable, and slightly more feasible, for the next one. At some point the question stopped being whether to have a derivatives desk and became, "How big do we want to go?"

Digital assets are following the same path, but faster. The repeal of SAB 121 and the creation of a US Strategic Bitcoin Reserve gave the asset class sovereign-level endorsement. Europe's MiCA took full effect. Dubai's VARA and Singapore's MAS granted full-scope licences.

Two of Asia's most significant developed markets are now doing the same.

In Japan, the FSA announced a reclassification of crypto assets, moving them from payments law into the Financial Instruments and Exchange Act, driven by recognition that digital assets are now held primarily for investment rather than transactions. The practical implication is that banks, insurers, and trust banks can begin treating cryptocurrencies in the same vein as stocks and bonds — a change in legal categorisation that determines what an entire class of institutions is permitted to hold.

South Korea is moving in parallel. The Digital Asset Basic Act acts as an umbrella law for digital assets, introducing measures covering stablecoins, digital asset ETFs, and blockchain-based instruments in public finance. From 2030, blockchain-based deposit tokens are set to be used for around 25% of national treasury payments, with a pilot launching in the first half of 2026.

A sovereign government routing a quarter of its treasury operations through digital infrastructure is taking a decisive step, not a bet. The Act also replaces the term "virtual assets" with "digital assets" across Korean financial law — a small detail that reflects a larger shift in how the state categorises what these things actually are.

Both Japan and South Korea are large, conservative, heavily regulated financial markets. Their moves carry different weight than a fintech hub issuing a sandbox licence. Add them to the US, EU, Singapore, and Hong Kong, and you have a near-complete sweep of the world's institutional capital operating from the same basic premise: that digital assets warrant proper regulatory architecture.

Individually, each development is incremental. Collectively they are not reversible.

So What is All This "Building" For?

Real-world asset tokenisation has grown 380% in three years to reach $25 billion, with Standard Chartered projecting growth to $30 trillion by 2034.

According to Coinbase's 2025 State of Crypto report, 76% of institutional investors plan to allocate to tokenised assets by 2026. Prime brokerage financing for digital assets, cross-margining between crypto spot and listed futures, tokenised government bonds settling on conventional rails — none of this is speculative. It is in production or undergoing active development at institutions whose names appear on fund prospectuses, not token whitepapers.

The FIX protocol was never built only for equities. It was built for any financial instrument that needs to be traded in a standardised, interoperable way. That crypto now runs through it is the protocol working exactly as intended, applied to instruments that happen to be digital.

The Question Has Changed

For a decade, the debate inside institutional investment committees was categorical: does this asset class deserve to exist in a serious portfolio? That debate is over, not because everyone is convinced, but because enough of the world's largest allocators have moved past it that the holdouts are increasingly the ones who need to explain themselves.

The question now is implementation. Sizing, access, risk framework, custody arrangement. That's a different conversation entirely — and once an asset class is being discussed in those terms by pension funds, sovereign wealth managers, and prime brokers, the direction of travel tends to be fairly predictable.

{kind=link}