Table of Contents

Bitcoin rose to a new high of over $50,000 on Monday, surpassing the year-high hit after the ETFs were approved in January. The largest cryptocurrency by market cap is also on track for its seventh consecutive daily increase. If this advance persists, it will be the longest such sequence since January 2023.

Additionally, crypto-related company stocks rose: MicroStrategy, Coinbase Global, and Marathon Digital all saw increases of 7.3%, 3.5%, and 8.3%, respectively.

But macro trends clearly point to easing global inflation and persistently strong economic activity, which the Organization for Economic Cooperation and Development (OECD) confirmed in its latest projections.

Surging inflation and higher interest rates were the bane for risk assets last year, but a turnaround in price pressures in recent months has added to investor's allure for higher-yielding assets.

Blockhead

Blockhead

Stocks Keep Rising Despite Central Banks' "Wait & Watch" Mode

A fresh surge in major tech and expectations that the Federal Reserve would soon be able to lower rates boosted the outlook for corporate earnings, leading Wall Street to a milestone as the S&P 500 surpassed 5,000 points on Friday.

A fifth consecutive week of gains was capped by equities' surge to a new all-time high as they closed out Friday.

Bets on a mild landing and the AI euphoria have driven the US benchmark gauge to more than quadruple from its pandemic low in March 2020.

The Nasdaq 100 rose 1% on Friday, with the most significant sector of the index, technology, driving the increase.

There is no better indicator of faith in the earnings capacity of American corporations or the health of the economy than the S&P 500. If profits and the economy are improving or worse, that will show up in the S&P 500's movement.

Investors can finally relax a few days before the crucial consumer price index (CPI) since a government report — typically disregarded by markets — confirmed easing inflation development at the end of 2023.

Federal Reserve Bank of Atlanta President Raphael Bostic expressed his "laser focus" on returning inflation to goal. In contrast, Fed Bank of Dallas President Lorie Logan expressed her lack of urgency in cutting rates.

That lines up with an OECD report which showed easing global inflation trend, but the international body warned central banks from declaring victory over inflation too soon.

More importantly, What comes next for the S&P 500 now that it has reached the 5,000-point mark?

The gauge's performance has been favourable after achieving key milestones. In the most recent nine instances, the index returned 10.4% on average during 12 months, with 78% of those instances yielding positive outcomes.

Proximity to this widely monitored threshold would generate headlines and amplify FOMO sentiments. Round figures, like 5,000, can potentially improve mood and serve as psychological support or resistance levels for the market.

If that level were to fail, it would become a new critical resistance level.

In any case, the stock market has had a fantastic surge this year. Therefore, in the grand scheme of things, it will only matter a little if any drop becomes a significant one.

Though some may dismiss it as insignificant compared to the plethora of numbers we encounter daily, this particular one holds some significance. The number five thousand does add to the anticipation since it signifies the start of a new millennium.

Accordingly, experts anticipate that the thrill will last for some time longer.

Forecast for corporate profitability is another reason the stock market has been strong to start the year.

Most earnings season has passed, and companies are significantly outperforming forecasts. Compared to the 74% average over the past decade, 80% of S&P 500 businesses have reported positive surprises in their earnings reports this earnings cycle.

In response, analysts are increasing their forecasts.

Following an initial forecast of only 1.2% growth in the fourth quarter, Wall Street anticipates an average increase of 6.5% for S&P 500 companies compared to last year.

This would be the greatest performance since mid-2022.

Still, given the current market conditions—low volatility, high interest rates, and 21 times forecast earnings multiple for US equities — bulls and bears are arguing over whether or not this surge can be sustained.

During the week ending February 7, the custom bull-and-bear indicator of Bank of America increased to 6.8. As a contrarian indication to sell, a score above 8 indicates that the bullish trend has gone too far.

Although the stock market seems overbought at present levels, many traders are afraid to lose out on potential future gains. This has led to a surge in popularity for options contracts that offer a little premium in exchange for a potential gain.

As pointed out by Susquehanna International Group, the premium in implied volatility of 3-month 10-delta options to 40-delta calls is now approaching its greatest level in ten years.

This correlation shows that more people are looking for call options that indicate larger gains than for options that indicate lower gains.

If they don't want to spend a fortune on benchmarks, traders are increasingly relying on the inexpensive contracts to set themselves up for large market advances.

In light of the intense responses to the Fed in the past several years, the stock market's resilience in the face of shifting Fed expectations and rising interest rates is noteworthy.

Despite a solid $25 billion auction that allayed fears of an excess supply, bond prices slumped.

Considering what transpired a year ago, investors are cautious as they brace for adjustments to the consumer price index.

While there is no serious reason to question the overall success of inflation, markets remain jittery despite a Friday's update confirming easing price pressures.

Treasury yields increased immediately following the release of the report, but they subsequently fell.

Following the Fed's "pivot" in December, the two-year yield returned to levels not seen since then.

But analysts warn with their age-old disclaimer: "Don't fight the Fed."

Blockhead

JP Morgan: Liquidity is the Biggest Worry for Uncertain 2024

A reason for concern is liquidity and volatility in the face of high global interest rates this year.

A JP Morgan Chase electronic trading study found that traders focus on dependable liquidity sources as they prepare for another year of volatility.

For the second year running, the yearly survey of institutional traders has shown that volatile markets are anticipated to remain the top daily difficulty.

Aside from data costs and regulatory changes, access to liquidity is the most pressing issue regarding market structure.

Another shock to the global economy may cause asset class volatility, which has been very muted recently, to rise.

Even though the study predicts both the Fed and the European Central Bank will cut interest rates by more than a percentage point in 2024, the most significant factor influencing market performance that year will be inflation.

According to JP Morgan, most respondents anticipate increasing their use of computerised trading platforms.

Most changes in electronic trading will be in corporate bonds, exchange-traded funds, and government debt.

Nevertheless, since the conviction of FTX creator Sam Bankman-Fried for fraud last year, institutional traders' enthusiasm for cryptocurrency has cooled, with 78% stating they have no intentions to deal in the market.

This is a significant increase from around a quarter two years ago.

When asked about technological trends that would affect trading in the future, traders again cited AI and ML as the most important factors.

That triumphed over blockchain technology and Application Programming Interface (API) integration, which enables programmes to collaborate.

Blockhead

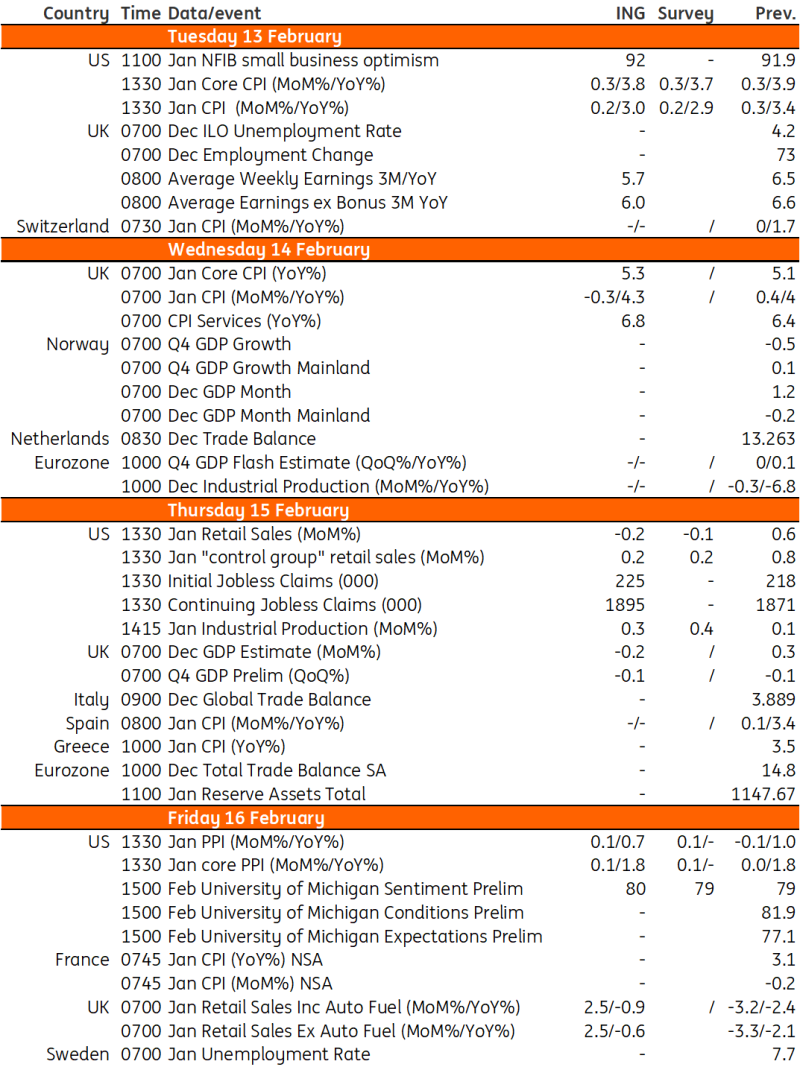

THE WEEK AHEAD

The main data highlights in the US this week will be the release of core inflation data along with retail sales, which are expected to come in soft given auto sale numbers.

That should draw eyeballs for those looking for cues on when the Fed will start its easing cycle.

In the UK, keep an eye out for a flurry of data releases including services inflation and wage growth - two driving factors for the Bank of England's next monetary policy decision.

Macro Data Calendar

Fed's New Test: "Broadening" Disinflation?

The likelihood of a Fed interest rate cut in March has been greatly reduced by the strong employment and GDP figures. Even May is not as clear as it was two weeks ago.

The possibility of monetary policy easing is still being considered, but policymakers have pushed back against the impression that it is imminent.

Reigniting inflationary pressures by easing monetary policy too soon is the last thing the Federal Reserve wants to happen at this critical juncture.

The best guess is that the Fed recognises its credibility was damaged by its "inflation is transitory" assertion in 2021 only to have to rapidly reverse course with significant rate hikes through 2022 and 2023.

A new criterion for interest-rate cuts appears to be a more widespread retreat in price pressures, which has shocked some Fed officials who were unprepared for the sharp decline in inflation in the second half of 2023.

The recent slowdown was driven more by goods, but last week, Boston Fed President Susan Collins and Richmond Fed President Thomas Barkin both made it clear that they want the inflation decline to continue and to expand more significantly to housing and other services.

This is in line with what many other officials have said: Postponing the initial rate cut until disinflation becomes noticeably more widespread is possible.

Fed Chair Jerome Powell has already stated that a rate cut next month is highly improbable, and policymakers have kept rates on hold since July.

Recent months have witnessed a significant improvement in inflation, which was further reinforced in revisions released on Friday.

This improvement may be attributed, in large part, to a turnaround in energy prices, the mending of supply chains, and decreased pricing for items such as secondhand automobiles and apparel.

Services inflation has also eased, helped by moderating wage gains amid an influx of workers into the labour market, but progress has been slower.

The consumer price index (CPI) is expected to have fallen below 3% in January for the first time in almost three years, giving Fed officials a new indication of inflation when it is released on Tuesday.

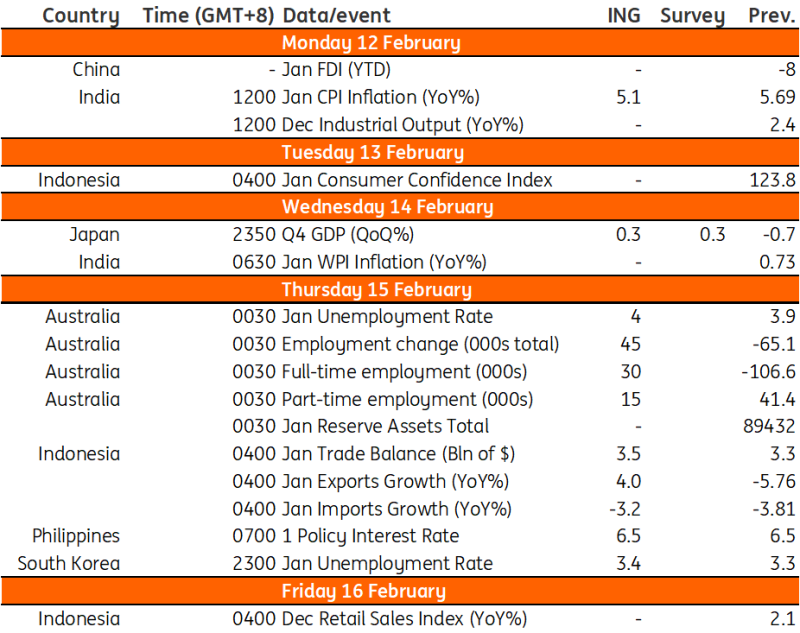

Asia Week Ahead

The latest jobs report from Australia features in this week's data calendar. Meanwhile, the Philippines holds a policy meeting and is expected to pause.

After the Reserve Bank of Australia paused but retained its slightly hawkish bias, this week’s employment data is important.

About the only good news last month was that a large drop in labour force participation helped to keep the unemployment rate unchanged at 3.9%.

Markets were emboldened to look for more and sooner RBA rate cuts than had been the case. That may not prove to have been a correct decision…the next inflation data will provide more insight.

Macro Data Calendar

Blockhead

Blockhead Blockhead

Blockhead

{kind=link}