Table of Contents

The Three Arrows Capital (3AC) bankruptcy papers include a wide range of bewildering conduct. Here we are going to zoom in on just the Greyscale Bitcoin Trust (GBTC) collateralized lending arrangements with Equities First.

There are widespread and confusing reports in the media about this. It feels unlikely 3AC is, on net, owed money by a business that describes itself as “an institutional investment firm that specialises in long-term asset-backed financing.” They are a provider of financing not a borrower.

And we have the details of those borrowing arrangements from court filings. On the basis of some calculations done below, it looks like Equities First mistook GBTC shares for actual Bitcoin and misvalued quite a few things. It is not possible to say this for sure at this point. But, on a spot-BTC basis all the loans were 50% loan-to-value (LTV) and the default notice was sent as soon as this passed 100%. But on a GBTC-share basis they were anywhere from 66–72% LTV and should have been liquidated 6 weeks earlier, during the Terra-Luna collapse.

Read more: What We’ve Learned From the Leaked 3AC Affidavit

If Equities First valued the collateral properly (as GBTC shares), 3AC should have been put into default immediately following the UST incident!

The Loans

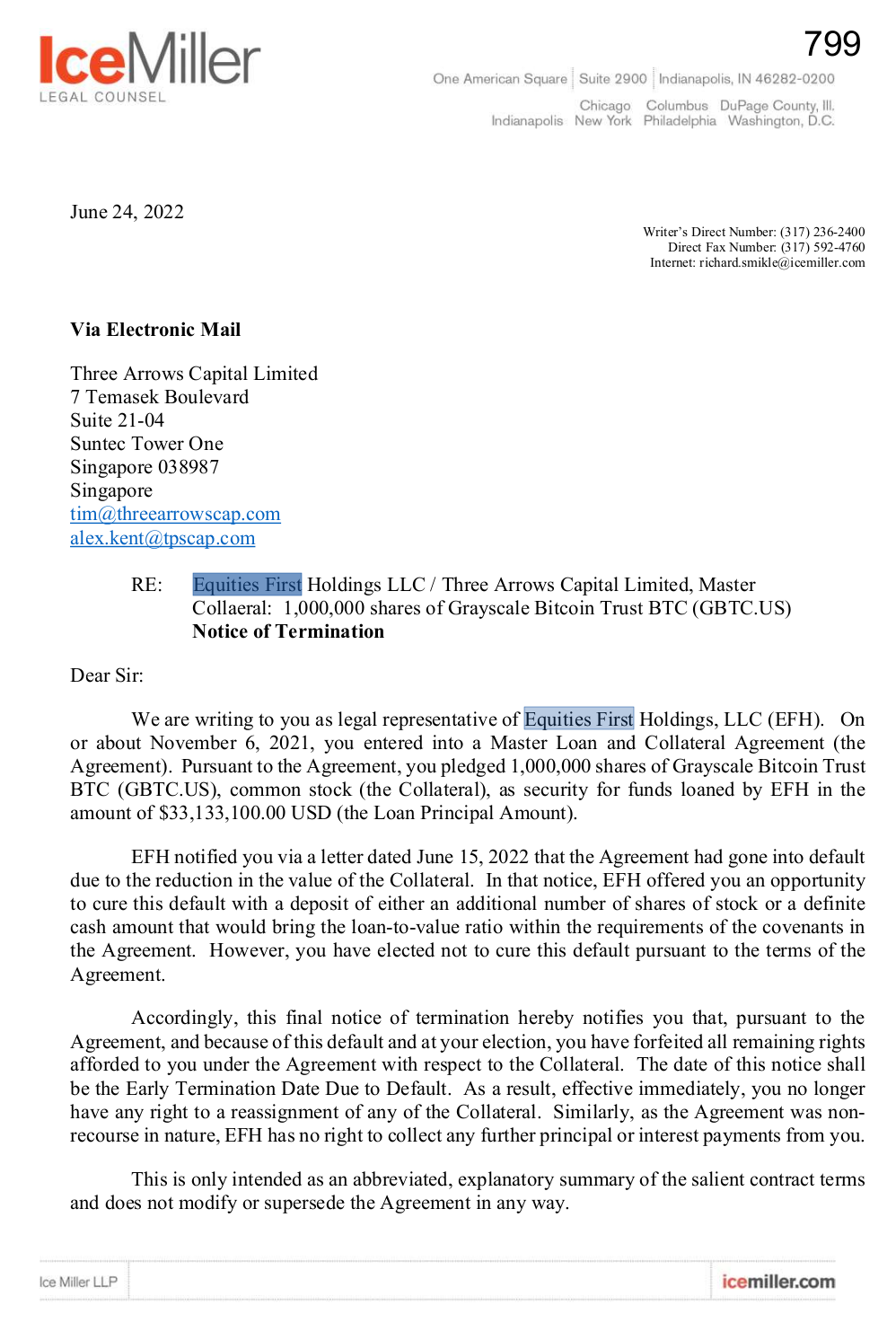

Here is one of the liquidation notices from the court filings:

There are three more. Recall that 1 GBTC share represents, sort of, 0.001 BTC. So a Bitcoin price of US$20,000 corresponds to something like US$20 plus or minus the premium/discount. We can consolidate all four loans into a table as follows:

| Date | GBTC Shares | $ Loan Proceeds | GBTC Price | BTC Price | LTV GBTC | LTV BTC |

| 6/11/21 | 1,000,000.00 | $33,133,100 | $48.57 | $61,539 | 68.2% | 53.8% |

| 11/12/21 | 1,500,000.00 | $38,841,600 | $37.28 | $50,149 | 69.5% | 51.6% |

| 2/1/22 | 2,000,000.00 | $45,745,300 | $34.25 | $47,299 | 66.8% | 48.4% |

| 8/1/22 | 2,000,000.00 | $44,339,500 | $30.74 | $41,685 | 72.1% | 53.2% |

We compute the “GBTC LTV” by dividing the loan proceeds by the product of GBTC price and # of shares pledged. And “BTC LTV” is computed the same way with the BTC spot price used in the denominator. The BTC market is volatile so don’t take all the decimal places seriously. But this sure looks like someone lending against spot BTC with a 50% LTV.

It is of course possible Equities First was trying to extend loans with 66–72% LTV and understood the differences between GBTC and BTC. But, as we will see below, the subsequent events are far more consistent with their misvaluing the collateral.

Default Timing

The aggregate position was a loan of US$162 million against 6.5 million GBTC shares. We can work out the 100% LTV liquidation price and compare that with the prices from a few dates easily:

| Date | GBTC Shares | $ Loan Proceeds | Implied Price | BTC Price | GBTC Price |

| 6/5/22 | 6,500,000 | 162,059,500 | $24,932 | $36,030 | $25.02 |

| 9/5/22 | 6,500,000 | 162,059,500 | $24,932 | $30,768 | $20.90 |

| 10/6/22 | 6,500,000 | 162,059,500 | $24,932 | $29,063 | $19.50 |

| 15/6/22 | 6,500,000 | 162,059,500 | $24,932 | $22,562 | $14.06 |

The period between the first two rows is the Terra-Luna incident. These loans were not exactly heavily overcollateralized before the incident. But during that collapse they went under. And Equities First did not ask for more money – per the information we have now – until 6 weeks later.

At that point they were underwater by something like 6.5 million * (24.932-14.06) = US$70 million before any losses on the liquidation. If this theory is correct they should have rung the bell on this mess when BTC was trading at 30k in mid-May!

Questions

This raises a lot of questions. First, it would be great to read the referenced “Master Loan and Collateral Agreement.” And one imagines the court documents will provide this eventually. But GBTC trades a non-trivial amount and Equities First is not a new business. Is there anything odd in the agreement?

Second, why are there widespread reports Equities First owes 3AC anything? Unless there is a lot more to the story – and again, they don’t appear to be a borrower – that is just 3AC misunderstanding that their collateral is gone. Or trying to somehow play the victim. Who knows.

Third, why does Equities First owe money to Celsius, as reported in the FT? That report suggests Celsius’ collateral got “trapped” somewhere. Having seen this 3AC confusion, one thought springs to mind: maybe Equities First again mistook GBTC for BTC, put the collateral tokens in, and then had a problem retrieving them. If anything like that happened it strongly suggests there are more GBTC horror stories to come out.

And finally, these documents strongly suggest 3AC was, properly measured and in a practical sense, insolvent as of the weekend of May 7-8. Whether they were legally insolvent with all that implies is a different question. But there were either some strange arrangements in place, some odd promises made, or some serious mistakes here.

Read more: “Please Let Us Know”: How Genesis Tried to Recover US$2.36B From 3AC

{kind=link}