Table of Contents

Hey there! Just a quick note to let you know that this edition of the Blockhead Business Bulletin is brought to you by our sponsor, Franklin Templeton. They're a global investment management organisation with over 75 years of investment experience. Being a California-based company, they offer value by leveraging its Silicon Valley roots and relationships with countless fintech, blockchain, and AI companies to bring insights directly to their clients. So, sit back, relax, and enjoy today's news knowing that it's made possible by our friends at Franklin Templeton.

CAPITAL FLOWS IN GLOBAL MARKETS

Those who predicted a weaker advance for the stock market this year are now upping their year-end projections for the S&P 500 Index.

Most experts have abandoned their 2023 price targets but have yet to be ready to become bullish.

Despite mounting evidence that the US economy may escape a recession — the pace of inflation has fallen overall, retail sales have remained robust, and the Federal Reserve is anticipated to maintain interest rates constant this week – strategists generally foresee a market slump in 2024.

The pessimism on Wall Street presents a predicament for investors with capital at risk.

Despite the Fed's best efforts, inflation remains an economic concern.

But equities survived similar challenges in 2023, and now some market observers are concluding that the bears will be incorrect again since Corporate America's earnings forecast is strengthening.

The Fed itself sees no symptoms of a recession. Not that there aren't some potential hazards, however.

If the economy and inflation don't slow down more, Fed members have indicated they are willing to raise borrowing prices again. Additionally, the bond market has never sounded recession sirens for such an extended period.

For equity investors, knowing exactly when the Federal Reserve would stop raising rates has historically resulted in returns in the double digits. However, the trajectory becomes unclear when the Fed pauses before resuming hikes.

Still, there are signs that investors have money to put to work in stocks.

Some of the capital looks to be flowing in from the wings. The economy is expected to have a gentle landing, which has led to the largest weekly inflow into equity funds in 18 months.

Wall Street Tumbles as Focus Shifts to Fed

Global stocks dropped as traders digested economic data and considered the effects of a strike on Detroit automakers ahead of the Fed's decision this week.

On Friday, major technology companies led the decline with more than 3.5% losses. This week's gains on the S&P 500 were lost, while the Nasdaq 100 fell by about 2%.

The announcement that Taiwan Semiconductor Manufacturing requested a delay in shipping high-end equipment sent a gauge of chipmakers tumbling.

The two automakers, Ford and GM, went back and forth. Bond yields increased. The currency hardly moved.

The VIX, Wall Street's most popular volatility indicator, rose from its 2020 low.

Recent economic data has strengthened the consensus that the Fed will keep its benchmark interest rate steady this week and stoked optimism that the central bank's tightening cycle may have ended.

The European stock market gained ground as trading ended, continuing a rise triggered by the European Central Bank's announcement that it would no longer raise interest rates.

The MSCI world stock index fell, while the pan-European STOXX 600 index gained.

Stocks from emerging markets rose, and MSCI's broadest index of Asia-Pacific equities outside of Japan ended higher.

$188 Billion Exodus From China

With so much money leaving the Chinese stock and bond markets, the country's economy is becoming more uncorrelated with the rest of the globe.

From a high in December 2021 until the end of June this year, foreign ownership in the country's shares and debt decreased by nearly 1.37 trillion yuan ($188 billion), or 17%.

That's before August's record $12 billion withdrawal from onshore stocks.

A housing market collapse, ongoing tensions with the West, and years of pandemic restrictions have all contributed to the "avoid China" theme becoming one of investors' most strongly held opinions.

Since 2020 ended, the percentage of foreign funds investing in Hong Kong stocks has fallen by more than a third.

Small-Cap Stocks Take Off

As we approach the fourth quarter of 2023, it is becoming evident that investing in the stocks of smaller firms is a successful strategy in developing economies.

So far this year, the strategy has generated relative gains of 12% above the MSCI large-cap index, which would be the second highest over the last 14 years.

The increased vulnerability of large-cap firms to China's economic slowdown is a contributing factor.

However, small-caps are doing well because of positive news about emerging markets like India and the current trend of investing in startups in emerging industries like artificial intelligence and electric cars.

There have been 14.7% gains in the 1,905 equities that make up the MSCI Emerging Markets Small Cap Index this year. That's in contrast to the large-cap sector, which rose 2.5% on average, where companies are valued at $7.9 billion on average.

High gains, however, come with increased danger for investors. Small-cap stocks in emerging markets are very sensitive to changes in risk appetite.

The MSCI small-cap index underperformed its large-cap sibling by almost 30% during the dot-com crash of 2000, the financial crisis of 2008, and the US-China trade war of 2018.

Dollar & Treasury Yields Gain

Two-year Treasury yields climbed over the 5% mark as investors fretted in anticipation that the Fed will keep rates higher for longer.

Yields on benchmark 10-year notes have increased from Thursday night's close of 4.29% to 4.3304%. The price of a 30-year bond dropped, increasing the yield to 4.4182% from 4.385%.

The dollar dipped slightly against a broad index of global currencies, but it still managed to post a weekly gain for the ninth week running.

The Japanese yen and the British pound lost ground against the greenback.

Oil Gains for Third Straight Week

As supply tightened, led by Saudi Arabian production cuts and confidence in Chinese demand, oil prices rose to a 10-month high on Friday and notched a third weekly increase.

In addition, oil prices are poised for their largest quarterly gain since the first quarter of 2022, just around the time Russia invaded Ukraine.

Since Saudi Arabia and Russia this month announced an extension of their joint production restrictions of 1.3 million barrels per day until the end of this year, supply fears have remained a major factor in the market.

Prices for a barrel of US crude oil rose to $90.77, while those for a Brent crude barrel gained $93.93.

In response to the dollar's weakness, gold prices soared, recovering from their lowest level in three weeks.

Bitcoin's First Weekly Gain Since August

Bitcoin reversed a four-week downtrend, but its sustainability is uncertain.

Since last Sunday, the market value of the cryptocurrency with the greatest market cap has increased by nearly 2%, to roughly $26,358.

THE WEEK AHEAD

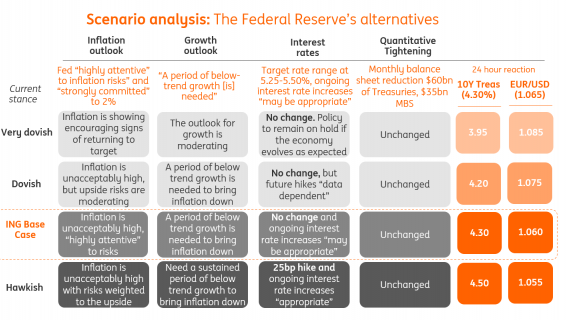

It's another week of central bank action, with all eyes on the Fed, which is predicted to stay on the sidelines but remain hawkish in its tone.

The Bank of England, on the other hand, is expected to hike rates, although a pause should not be ruled out.

Fed Set to Signal the Potential for a Final Hike

Inconsistent US data and Fed remarks lend credence to the market's price of another pause at the FOMC policy meeting on September 20.

While markets don't expect the Fed to implement a last rise, inflation worries and economic resiliency indicate it may do so anyway.

Officials' comments, even from hawks like Neel Kashkari, imply a readiness to pause in September (as it did in June) but to keep the door ajar for a further raise at the November or December FOMC meetings.

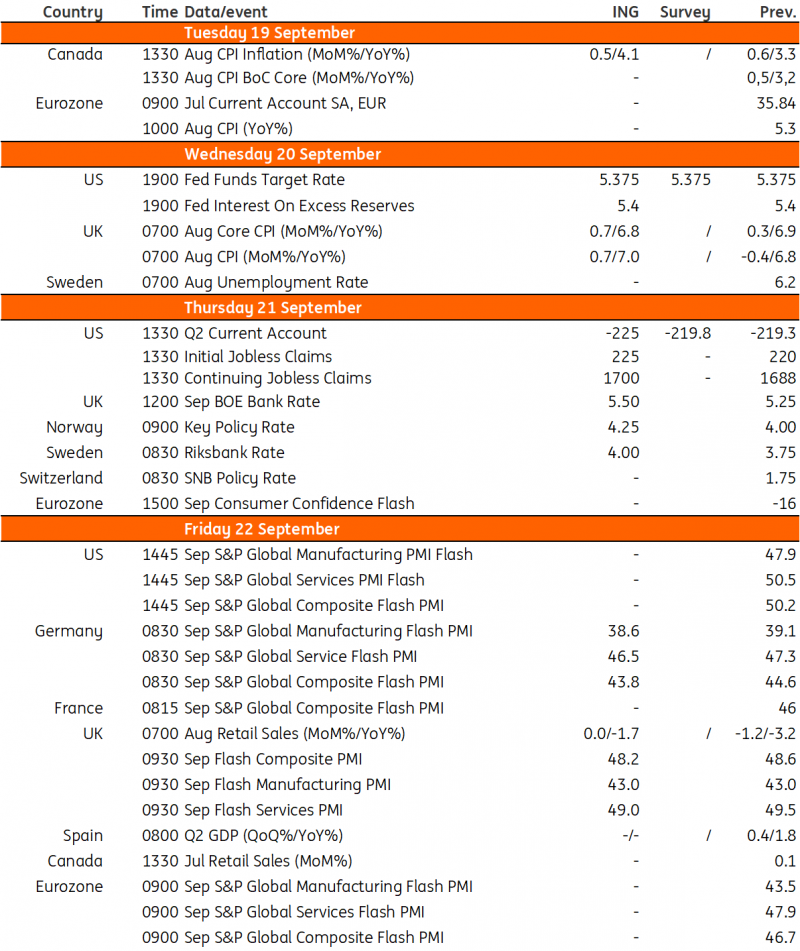

Key Events in Developed Markets

- US: Fed to Leave Interest Rates on Hold

- UK: Bank of England to Hike Rates Further, But Don’t Rule Out a Pause

- Norway: Norges Bank Set for a Further Hike

Macro Calendar

The potential for further Fed hikes remains, with the dot plot to retain a final hike – but markets don’t see it being implemented.

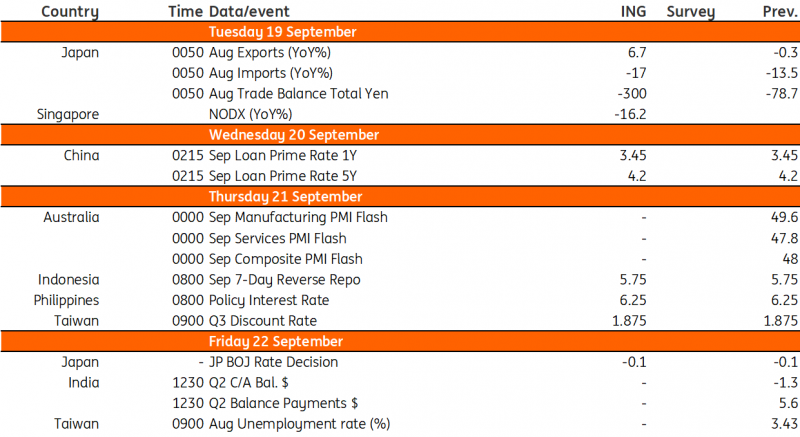

Key Events in Asia

Central banks in Indonesia, Japan, the Philippines, and Taiwan will hold their respective policy meetings this week. China will also be announcing its 1-year and 5-year LPR rates.

Asia Week Ahead: Key Regional Central Banks to Decide on Policy

- China's 1-year and 5-year LPR rates to remain unchanged

- Regional central banks to stand pat

- Inflation and trade figures for Japan

Macro Calendar

In Asia too, all eyes will be on what the Fed does this week.

There has been talk of a change in the Federal Reserve's long-term prediction for the appropriate Fed funds target rate level.

This is a major development due to its support for rates on longer-term Treasury securities. This has been consistently estimated as 2.5%, but recently, several people have shifted their estimates upwards.

The tide is favouring a shift from the Fed.

Blockhead

Blockhead

{kind=link}