Table of Contents

In the dynamic and ever-evolving landscape of global financial markets, Malaysia finds itself standing at the precipice of a new era – the one of Initial Exchange Offerings (IEOs). This emergent financial technology promises to revolutionize the way companies raise capital, offering a new avenue for growth and innovation. Yet, the nation's journey into this uncharted territory is not without its share of turbulence and uncertainty.

At the heart of this maelstrom stands the Malaysian Securities Commission (SC), the vanguard of the financial realm. Its actions and decisions, often shrouded in a veil of regulatory jargon, are shaping the course of this nascent industry. The SC's mandate is a noble one: safeguard the interests of investors and ensure the stability of the financial markets. However, the question arises – are their regulatory actions truly protective measures, or are they merely veils masking a lack of understanding of this emergent financial technology?

Historically, the SC has been a cautious entity, often trailing behind the global curve in accepting financial technology by a few years. This conservative approach, while prudent, has inadvertently fostered a phenomena of "learned helplessness" within the private sector. The innovation engine, once roaring with potential, now finds itself muffled under the weight of regulatory inertia, its spark dimmed by the lack of foreign investment.

Edmund Yong, founder of Celebrus Advisory, a seasoned player in the blockchain arena, observes, "The SC is playing it safe, their efforts in regulation are akin to motherhood and apple pie." His words paint a picture of a regulatory body that is cautious, perhaps overly so, in its approach to new financial technologies.

The SC has placed responsibilities of due diligence to IEO operators and placed themselves at the last mile of approval, where issuers are also required to submit a white paper to the SC.

Yet, the guidelines are as vague as a monsoon cloud, offering little insight into the approval process and a disclaimer at the very end that says: "The furnishing on this white paper to the Securities Commission Malaysia should not be taken to indicate that the Securities Commission Malaysia assumes responsibility for the correctness of any statement made in this white paper."

"The complexities of IEOs seem too difficult for the SC to handle," Yong remarks, highlighting the nebulous nature of the recent regulatory document on IEOs.

This lack of clarity, coupled with the requirement for issuer applicants to have RM 500,000 (~US$108,600) in paid-up capital, creates a formidable barrier to entry for most companies, let alone growth startups. It skews the playing field in favour of medium to large-sized companies, leaving the smaller players pushing forward innovative business models out into the cold.

Yong points out the misalignment in product-market fit, stating, "Private tokens are not listed anywhere else, IEOs use fiat to crypto transactions and are not crypto-native, there's a lack of systems in the ecosystem."

How Much Investor Protection is Too Much Investor Protection?

Yet in order to cross the unknown in this cosmic voyage to gain some sense of the world, the SC and IEO operators have laid out technical rules that would raise some eyebrows.

For issuers, the funds raised through IEOs platforms will be kept with a trustee and the issuers will receive the funds only after achieving planned milestones. The milestones here are set by the issuer in their submitted business plans and approved by the IEO platform. The funding schedule on the other hand is set by the SC as a pseudo investor protection if things go south.

For investors, retail investors have a maximum allocation of RM 2,000 ticket sizes per IEO round. However, these limitations do not exist for investments from institutions, HNWI, and family offices.

Assuming all things equal and go according to plan, this leaves a gap in product-market fit as any logical investor would rather choose a more competitive product in convertible notes from the startup over tokens. The upside caps on investors here not only discourage foreign investment but also leaves investors in a state of limbo, unable to anticipate its chance to liquidate holdings into a secondary market.

Misalignment in Product-Market Fit?

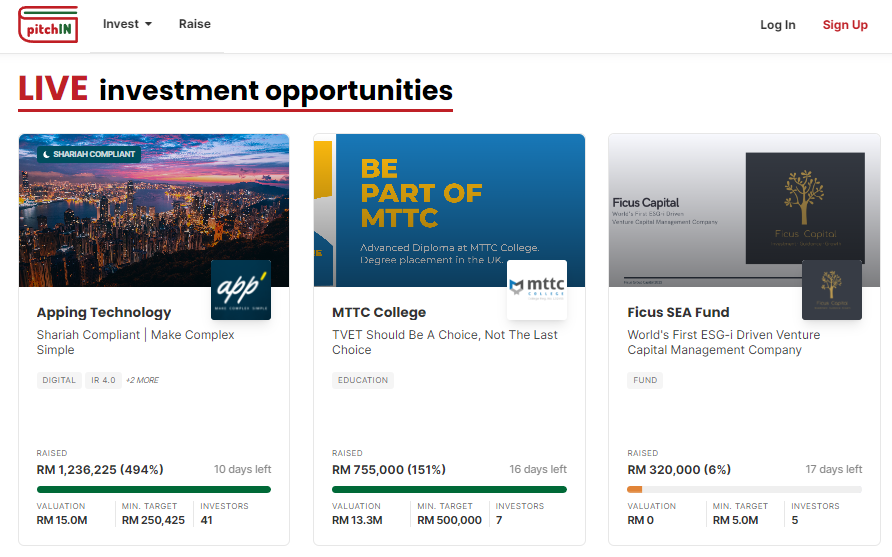

In the grand tapestry of Malaysia's financial landscape, two entities stand out, weaving their unique threads into the intricate design of IEOs: PitchIn and KapitalDX. These two IEO operators, each with their contrasting offerings, are poised to play a pivotal role in the unfolding narrative of this emergent financial technology.

PitchIn is an RMO-IEO operator licensed by the SC. Their platform, while still in its nascent stages, promises to offer investors a direct window into the world of business models implementing their way to Web3. The challenge, as COO Wei Chi Chan sees it, lies in user onboarding and trust-building as they introduce this new asset class for issuance on digital tokens.

Yet, PitchIn is not daunted. They are taking a bold step towards introducing new asset classes, hoping to attract a new breed of investors from all corners of the country and globe. Their focus is on issuers with existing proven models that are incorporating blockchain tech to make their business more exciting and innovative. More importantly, these issuers already have an existing client base and generating revenue, making it easier to gain more users by providing them a strong offering.

"Our strategy here is to test the waters first. The first year is not intended for massive growth, but rather to understand the market dynamics and adapt accordingly. We are taking a long-tailed approach, as we are looking for companies that are transitioning from Web2 to Web3. It's a cautious yet ambitious approach, reflective of achieving the needs of market before we can move towards a vibrant marketplace for these type of issuance," said Chan.

On the other side of the spectrum is KapitalDX, helmed by CEO Selvarany Rasiah. This RMO-IEO operator, already licensed by the SC, has a live platform but is yet to hold an issue note for investors. They are expecting to launch their first note by Q3 2023.

KapitalDX takes a more conservative approach, opting to focus on models that use the novelty of the blockchain, offering investors a secure and transparent window to asset ownership, using blockchain technology in traditional products. They view the IEO as a novel fundraising mechanism, opting to serve revenue generating companies hungry for scale.

In our interview, Rasiah said that they intend to open up their doors to prospects that live in the realm of Series A and beyond. Alternatively, financing projects that have a profitable record and are ESG-friendly (Environmental, Social, Governance).

Their approach is one of caution and meticulousness. They emphasised that all legal rights and thorough contractual agreements are in place for investor protection. They are looking to fill a growing funding gap worth RM 90 billion in the Malaysian ecosystem and seek to bring investors along by giving them access to private market assets, previously enclosed to high-net-worth individuals (HNWI) with big ticket sizes and institutions.

But What About Due Diligence?

While these plans of the operators are lofty and sound as satisfying as rain hitting rooftops, the brass tacks come down to how due diligence is conducted. In the house where the facilities for IEOs are non-existent, who keeps these operators in check, and why does the regulator choose to implement IPO practices on growth stage companies?

Past IEO initiatives in countries around the APAC region since 2019 have concluded that too much regulation impedes growth on innovation. The SC is sitting on the comfort of their highest levels of training while taking stabs in the dark with a wait-and-see approach.

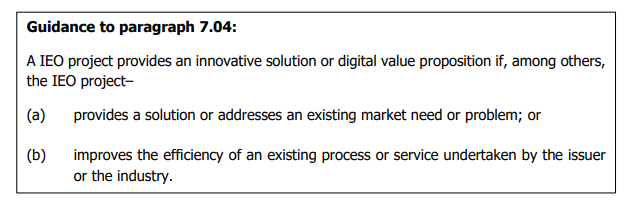

Moreover, the SC criteria for "qualified applicants" is equally ambiguous. The demand for an "innovative solution or meaningful digital value proposition or addressing an existing market need/problem" is as wide as the horizon, leaving applicants adrift in a sea of uncertainty.

However, both Chan and Rasiah mentioned that the onus on due diligence responsibility is at a standard in conjunction with the SC's requirements. Security tokens issued on IEO platforms are deemed securities by Malaysian law and are inline with securities regulation.

Each said that they have two separate due diligence processes; a standard due diligence method and a token economics evaluation method. Chan deriving experiences from running an equity crowdfunding platform, and Rasiah from her extensive experience serving as the former Chief Commercial Officer for the Malaysian Stock Exchange, Bursa Malaysia.

Whether these methods and learned experiences prove to be effective, it remains a sight to behold if the weight of responsibility can be supported by the shoulders towards a market of possibility. Or if said weight breaks the camels back.

Final thoughts

"There aren't enough crypto accountants and valuators. We need prescriptive regulatory guidance," says Yong in relation to what the Malaysian ecosystem needs.

His words echo the sentiment of many in the industry, who are calling for the SC to shed its conservative cloak and embrace the potential of IEOs. To do so, the SC must not only understand the intricacies of this new technology but also foster an environment that encourages innovation and growth. This involves providing clear and comprehensive guidelines for IEO operators and applicants, ensuring that the approval process is transparent and fair.

The current state of the IEO landscape in Malaysia is a paradox. On one hand, it offers a beacon of hope for companies seeking to scale and expand beyond national borders. On the other, it is a labyrinth of vague regulations and unclear policies, with no secondary marketplace to facilitate trading. This dichotomy is a reflection of the broader challenges faced by the Malaysian financial markets as it grapples with the rapid pace of technological change.

As we stand at the crossroads, it is crucial to question and empathize with the practices of the SC. The future of the Malaysian financial markets hinges on the SC's ability to adapt and evolve, to shed the cloak of ambiguity and don the armor of clarity. Only then can the nation truly embrace the promise of IEOs and stride confidently into the future.

In the words of Alan Watts, "The only way to make sense out of change is to plunge into it, move with it, and join the dance." Both PitchIn and KapitalDX are doing just that. They are not merely spectators in the unfolding narrative of IEOs in Malaysia, but active participants, each dancing to their own rhythm, yet moving in harmony with the music of innovation and growth.

They represent the potential of IEOs in Malaysia, embodying the spirit of innovation and the promise of growth. Their journey, much like the journey of IEOs in Malaysia, is just beginning. And as they dance to the rhythm of change, they invite us all to join in and be a part of this exciting new chapter in the history of financial markets.