Table of Contents

This column is fond of pointing out that a lot of what happens in crypto is not particularly new to finance in general. Though we did find an example a few months ago concerning Gemini that was new, if not necessarily in good ways.

The FTX/Alameda debacle looks a lot like a blend of three financial train wrecks from about 30 years ago. And it blends the worst attributes of each into a particularly repugnant tale of woe that will surely go down in the annals of financial history.

Yamaichi Securities

Yamaichi was a major broker in Japan, one of the four big brokers during Japan’s epic 1980s bull market (bubble). As Yamaichi’s clients suffered large losses during the unwind of that bubble, their broker set up what is known in Japanese as a “tobashi” scheme. This is a broad class of scheme where a bank or broker tells clients it will guarantee certain trades do not make losses and does so by promising to buy back anything they need to sell at the original price.

A simple crypto tobashi might involve someone selling you Bitcoin at some price and promising to buy it back at that price in the future if you need to avoid a loss. Clearly this just dumps the loss on whoever is making the guarantee. And this sort of thing always blows up eventually.

In the case of Yamaichi, a business magazine exposed in 1997 that the firm had absorbed over US$1 billion dollars in losses via such a scheme. Remember this is a Japanese broker nearly 30 years ago – that was a debilitating loss. And Yamaichi went under. Importantly, the scheme itself was not the proximate cause of the failure, rather things unravelled quickly once the scheme was exposed. A similar arrangement at Olympus ran for decades and we do not really know all of the details even now, 10 years after it blew up.

The key point here is that the scheme blew up quickly once it was exposed, rather than collapsing under it’s own weight. Yamaichi failed and creditors experienced losses. For Japan, this was jarring and Yamaichi’s last president offered a tearful apology to the public (as is tradition in Japan for such things).

FTX was not exactly guaranteeing Alameda would not incur losses – it was simply financing Alameda’s ever-growing losses. But, in an incredible parallel to Yamaichi, an already-gone company only blew up when the public found out.

Israeli bank stock crisis

Also in the 1980s, Israel went through a financial crisis that involved most of the country’s major banks. The Bank of Israel produced a wonderfully detailed report on this crisis long ago that is surely worth a read. But the essential points are as follows:

- Bank managers wanted to ensure their stock price was high (normal).

- They encouraged clients to buy their stock (OK).

- They guaranteed those investments would not lose money (not OK).

- Loans were offered to facilitate these “can’t lose” purchases (disastrous).

Notice this is not precisely the same as Yamaichi. And – this is important – these schemes collapsed under their own weight when the banks ran out of capital to fund purchases and loans.

As the entire banking system was at risk the government stepped in and bought up the banks’ outstanding, collapsing, shares. Most of the banking system was taken in to public ownership, executives went to prison, and Israel’s banking system today is considered very healthy.

Here the FTX/Alameda similarity is glaring. Per the New York Times‘ reporting, they had been borrowing client funds to cover losses for months. Israeli banks were not gambling with client deposits. But they were, importantly, constrained in how much money they could get their hands on to support the stock by regulations linked to those deposits. That the Israeli banks did not completely implode and take customer deposits with them was a triumph of the regulatory system. At the same time, of course, that they were able to get there at all was a large failure.

FTX’s ultimate problem was that they could only “borrow” so many customer funds before the customers noticed their withdrawals not working. They dug deeply into the client funds before anyone noticed primarily because nobody was looking.

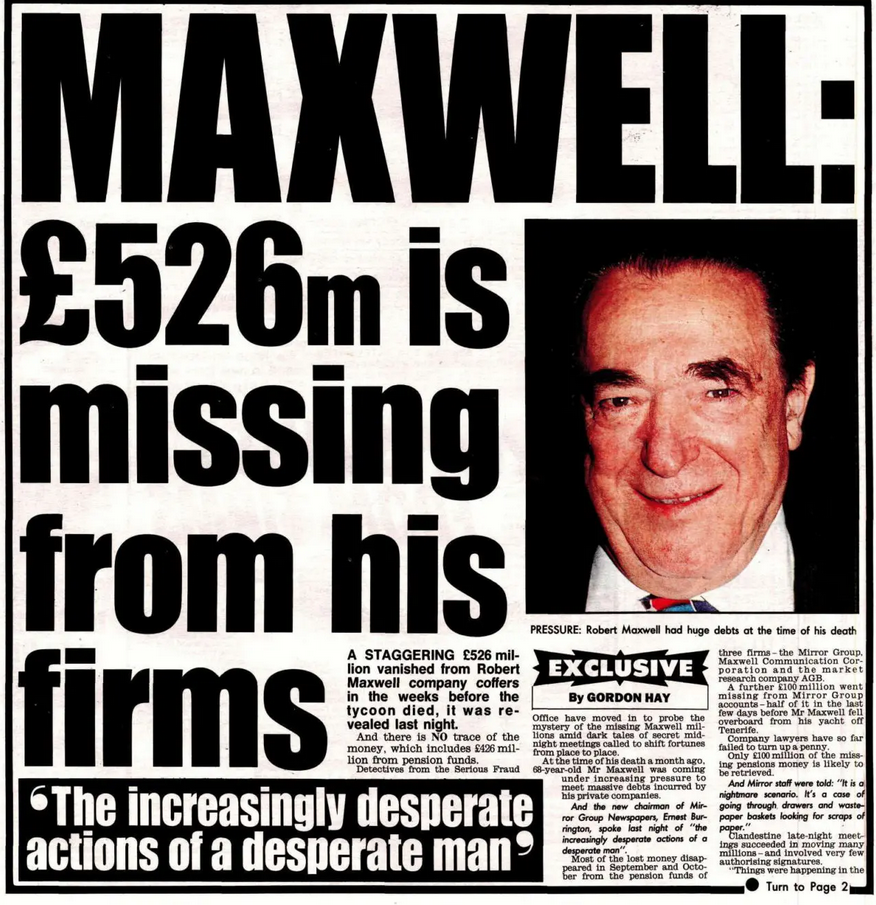

Robert Maxwell

The third old parallel is the Robert Maxwell scandal. The first thing to note here is that this obituary from 1991 makes no mention of the scandal. His business career is lauded. And what there is criticism focuses mainly on his personality and penchant for litigation. But this article in the same newspaper from 2011 is entitled “Pension plunderer Robert Maxwell remembered 20 years after his death.” Now you can read the wiki biography. The man died a hero and his misdeeds were only discovered when his empire crumbled due to fraud.

Robert Maxwell stole – stole, read the transcript of this recent talk by one of the trustee’s involved – a lot of money. He did so by simply taking assets from his company’s pension funds and using them for his own varied purposes. But, because he took them from the pension funds and supervision was lax, nobody noticed. Pensioners cannot call up their fund and ask for the money early.

All of this only emerged following his death. Nobody knew these funds were insolvent while he was alive. The scandal was not only shocking, it was a genuine surprise. Rumours of financial trouble had dogged Maxwell for years. But it was the 80s and he was large-personality financier: that was nothing new either.

Again, as with the Israeli bank situation, a large number of members of the public were impacted and the government did something. While they did not fully bail out the failed pensions they contributed some funds and only fully extricated themselves from the mess this year.

FTX/Alameda managed to misappropriate perhaps more than US$10 billion dollars worth of assets without anyone noticing until a liquidity crisis destroyed the firm in a week. But following the death (in this case of firm rather than founder), ever larger losses are emerging.

The Trifecta

The FTX/Alameda implosion borrows the worst attributes of these three incidents. Money was stolen. Losses emerged following an unexpected collapse. Those losses happened quite some time ago and were covered up. And while the scheme unravelling did lead to the bankruptcy of the involved entities it did not exactly collapse under its own weight. Rather it was the public’s discovery of the problem that led to the bank run which killed the firm.

And, unlike any of the cases discussed above, no government is going to bail these folks out. Yamaichi did not vanish along with all it’s client’s assets even while the stock went to 0. The Israeli banks inflicted losses on the taxpayers (and a bit of a currency devaluation). And Maxwell’s pensioners ended up with partial coverage. The burden was shared in some odd way and reforms were instituted.

Here the burden will be imposed on FTX’s depositors and Alameda’s lenders. And it very much remains to be seen if any reforms will come about.

Related: FTX: WTF?

{kind=link}