Table of Contents

Kevin Warsh’s first Federal Open Market Committee meeting was never going to be quiet. The Fed held its benchmark rate at 3.50%–3.75% on Wednesday, a decision that arrived with near-universal expectations of a pause. What nobody had fully priced was the force of what followed: nine of 18 FOMC members now project at least one rate hike before year-end, the median dot climbed to 3.8% from 3.4% in March, and Warsh announced at his first press conference as Fed chair that the institution had dropped forward guidance entirely. The 2-year Treasury yield spiked 17 basis points to 4.22% — a level that now sits above the top of the Fed’s own target range. The Nasdaq fell 1.35%. Bitcoin declined roughly 1% to around $64,300.

The hold was never the story. The story was that Warsh used his debut to do something no Fed chair had done in years: shift the institution’s operating posture rather than simply validate the consensus.

For most of the post-pandemic period, the Fed communicated in advance. Rate guidance was explicit — “higher for longer,” “data-dependent,” “we’re near the peak.” Under Powell, forward guidance was the primary instrument through which the Fed managed financial conditions without moving rates. Warsh has now explicitly abandoned that model. By declining to submit a dot plot projection himself and announcing the removal of forward guidance as institutional policy, he has signalled that monetary policy will be harder to trade around. Markets can no longer anchor to a known easing path. That, on its own, represents a meaningful tightening in financial conditions, independent of any actual rate move.

The inflation backdrop made this shift possible. Core PCE has been revised to 3.3% for 2026, up from the 2.7% projected in March — a material change that reflects both an energy price shock and a labour market that has stayed stronger than most forecasts assumed.

Warsh’s comment from the press conference was characteristically direct: “We’ve missed on inflation for five years and we’re going to fix that.” Fitch, reacting to the decision, noted that the inflation fight remains structurally intact, and that the revised dot plot is consistent with a central bank treating credibility as the primary asset to protect.

The rates-crypto correlation

The market’s immediate reaction in crypto was contained but pointed. Bitcoin’s roughly 1% decline looks modest set against FOMC meetings in 2022 and early 2023 that sent the asset down 5–8% on intraday moves. But the signal embedded in ETF flows was sharper: Bitcoin and Ether ETFs combined for $111 million in outflows in the immediate aftermath of the decision. That number reflects institutional positioning. The capital moving out was reducing risk exposure in response to a macro signal.

The rates-crypto correlation has been debated throughout 2025 and into 2026. Bitcoin’s rally from late 2024 through early this year occurred in a macro environment that was neither cutting aggressively nor hiking — a period of benign drift in which crypto attracted capital on its own narrative: ETF inflows, institutional adoption, halving dynamics. Wednesday’s FOMC did not end that narrative. But it reintroduced a constraint that had faded from the conversation: the opportunity cost of holding Bitcoin against a 2-year Treasury yielding 4.22%.

That yield figure is not incidental. The 2-year now sits above the top of the Fed funds target range, which means the bond market is pricing in something incrementally more hawkish than the Fed’s own stated policy. At 4.22%, short-dated Treasuries offer risk-free duration that competes directly with the kind of capital allocation that flows into Bitcoin and digital assets more broadly. In 2022, when the 2-year moved from near zero to above 4%, it corresponded with Bitcoin’s worst calendar year on record. The mechanism is not identical today — BTC’s institutional base is deeper, ETF wrappers have broadened access, the asset has a clearer macro identity as a hedge — but the basic dynamic hasn’t been repealed.

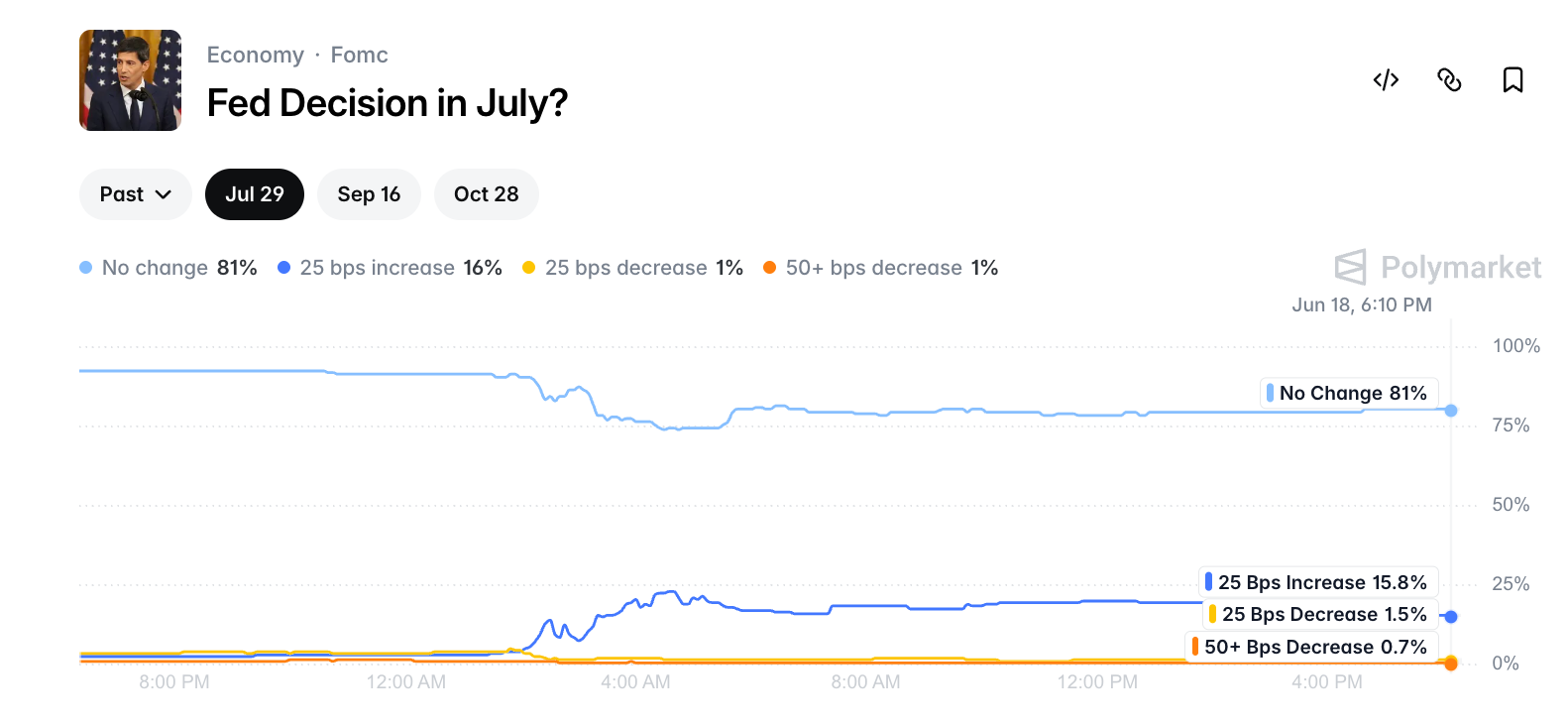

July is not the consensus call. Markets are now pricing a hike at that meeting with roughly 16% probability, up 13% before Wednesday, per Polymarket data. October sits closer to 60%. The gap matters because it gives the Fed data — two CPI prints, two jobs reports, one PCE release — before it has to commit. If inflation continues printing above 3%, the October hike becomes the base case. If it recedes, Warsh has preserved enough optionality to hold again without appearing to capitulate. Dropping forward guidance was, among other things, a mechanism for preserving exactly that flexibility.

For crypto markets, the near-term question is whether the post-FOMC repricing is a single-session event or the beginning of a sustained macro overhang. The answer likely depends less on the July meeting and more on whether core inflation starts to print lower. The energy shock that pushed prices higher this spring is transitory by nature. If it fades, the case for a hike weakens and crypto’s correlation to rates becomes less punishing. If it proves stickier — or if the services component of core PCE re-accelerates — Warsh’s “fix that” framing will be tested in a way that requires an actual rate increase, not just a hawkish press conference.

Wednesday did not represent a regime change for digital assets. But it ended the period in which Bitcoin could be discussed as though macro conditions were a secondary variable. Warsh’s Fed has made clear it is not operating on a predetermined path. That ambiguity has value for the institution — and a cost for risk assets that had grown accustomed to trading the forward curve.

{kind=link}