Table of Contents

The recent alignment of Bitcoin with US tech stocks appears to stem from a common vulnerability to macroeconomic factors, rather than indicating any fundamental similarity between the two.

The recent rise of Bitcoin in parallel with the tech-heavy Nasdaq has led many to speculate that Bitcoin is a metaphor for the whole technology industry.

Analysts say that despite the strong connection between their indexed values, claiming that software stocks and Bitcoin are fundamentally aligned or are similarly impacted by topics such as AI or quantum danger is exaggerated.

The simultaneous rise likely indicates a common vulnerability to the prevailing macroeconomic environment, particularly concerning long-duration, liquidity-sensitive risk assets, rather than suggesting a fundamental alignment between Bitcoin and software stocks.

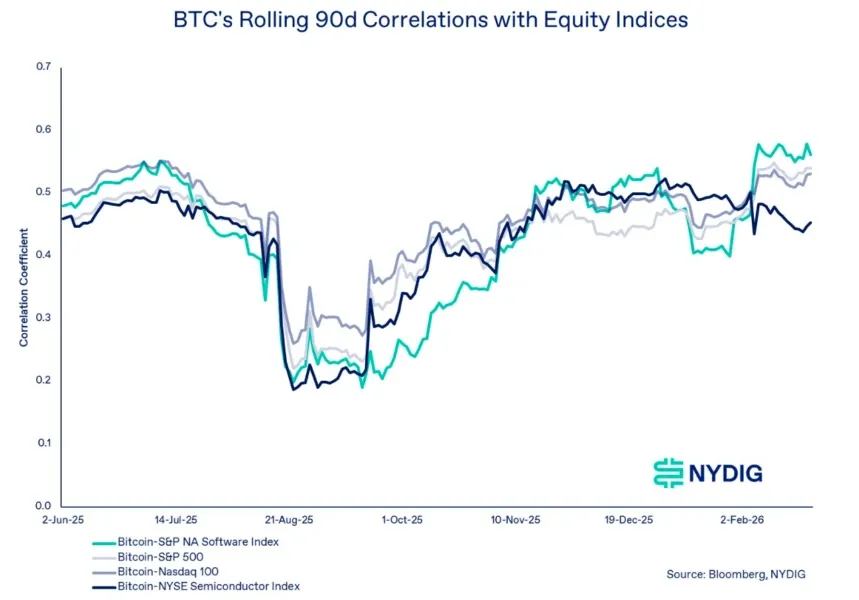

During the last three months, from early October, when it surpassed $126,000, the correlation between tech equities and Bitcoin has become stronger.

Its recent spike in linkages with the Nasdaq and the S&P 500 further suggests that this movement is not limited to software stocks.

Still, a large chunk of the volatility in Bitcoin's price cannot be explained by stock market factors, even if there are correlations between the cryptocurrency and software stocks and the two indexes.

The correlation between Bitcoin and the stock market accounts for just a fourth of its price volatility; the remaining three-quarters is caused by variables unrelated to traditional stock indexes.

The ongoing dissatisfaction with Bitcoin's performance, despite being called digital gold, appears to stem from the fact that it is not seen as a hedge against larger economic forces.

Investors seem to be directing their funds towards assets across a spectrum of risk, instead of purchasing Bitcoin based on a clear monetary rationale.

However, Bitcoin stands apart from other assets because of its distinctive market structure and economic characteristics, which are highlighted by its network engagement and adoption patterns and by legal and policy developments.

This differentiation emphasizes the importance of Bitcoin as a portfolio diversifier.

The current state of the linkages between various asset classes and stocks does not, however, guarantee that they will influence Bitcoin's yields.

Bitcoin is commonly seen as a leveraged technology investment with a high degree of risk because of its sensitivity to changes in liquidity, interest rates, and investor emotion.

When Bitcoin rose while tech stocks faltered, it demonstrated its ability to operate independently, reflecting the occasional brief decouplings that can occur in the market.

But Bitcoin often moves in tandem with tech equities. This component is unique and highly volatile within a well-rounded investment strategy due to its strong correlation, often exceeding expectations, and the presence of its own influencing factors.

According to Barchart's findings, the software growth dynamics domain is beginning to place a higher importance on Bitcoin. Because long-term SaaS providers are vulnerable to changes in borrowing rates and liquidity, there is a strong link (about 0.73) with the iShares Expanded Tech-Software ETF.

Grayscale had a correlation of 0.12 with gold in early 2025, but a far stronger connection of 0.68 with the Nasdaq-100 over the course of 90 days.

Due to unique circumstances in the cryptocurrency market and particular changes in US trade policy, this connection temporarily dipped into negative territory (-0.24) near the end of 2025, reaching yearly lows.

The Correlation's Key Drivers

Bitcoin and technology stocks are often regarded as volatile investments that typically decline when the Federal Reserve raises interest rates, yet they usually enjoy significant growth during periods of quantitative easing.

Bitcoin is now considered a "growth" or "innovation" asset class due to the participation of institutional investors like BlackRock's IBIT ETF.

Bitcoin serves as a continuously accessible liquid collateral asset. During a downturn in technology shares, individuals may convert their Bitcoin holdings to meet margin requirements, resulting in a self-reinforcing cycle.

But the yearly performance over the last two years spells out a different view.

Comparative Performance in 2024 & 2025

Year Bitcoin Return Nasdaq-100 Return

2024 +135.04% +33.57%

2025 -17.16% +6.78%

Having said that, the surge in adoption of crypto as an investment bet has boosted that correlation with several tech stocks.

A number of particular tech stocks have high correlations with Bitcoin, due to their large Bitcoin holdings or their involvement in maintaining the vital crypto economy infrastructure. These companies are highly dependent on the value of Bitcoin due to the token's substantial exposure on the balance sheet. They are also known as "proxy" stocks for crypto.

The performance of stocks related to crypto infrastructure and exchanges is closely linked to trading volume and the mood of retail investors, often experiencing significant increases in tandem with the price movements of Bitcoin.

Companies with a diverse income stream and positive ecosystem impact are known as indirect "Enabler" stocks, and their correlation is "softer" or more variable because of it.

As the debate rages on, soon the distinction will start to diminish as Wall Street embraces crypto in a more expanded way.

Blockcast – Licensed to Shill: Designing Decentralization: Governance, Power, and the Validator Problem

This episode examines what happens when decentralization moves from whitepaper language to operational reality. Tanisha Katara joins the discussion to unpack three structural tensions inside modern crypto governance: validator power concentration, voter apathy, and the emerging role of AI agents in decision-making systems.

If you enjoyed this episode, please like and subscribe to Blockcast on your favorite podcast platforms like Spotify and Apple.

Blockcast is hosted by Head of APAC at Ledger, Takatoshi Shibayama. Previous episodes of Blockcast can be found here, with guests like Fredrick Gregaard (Cardano Foundation), Daren Guo (Reap), Yat Siu (Animoca Brands), Kean Gilbert (Lido), Joey Isaacson (Nook), Kapil Dhiman (Quranium) Eric van Miltenburg (Ripple), Davide Menegaldo (Neon EVM), Anastasia Plotnikova (Fideum), Jeremy Tan (Singapore parliament candidate), Hassan Ahmed (Coinbase) and more on our recent shows.

Be at the heart of TradFi–DeFi collaboration at Money20/20 Asia 2026.

Are you looking to forge partnerships with banks and fintechs? To expand into new markets across Asia, or to secure funding from top-tier investors? This April, the world of digital assets, blockchain, and Web3 converges with the biggest players in APAC’s financial ecosystem at Money20/20 Asia 2026 and its brand new ‘Intersection’ zone, complete with a dedicated content stage, TradFi-Defi innovator showcase, and curated networking spaces. From traditional banking giants to decentralised innovators, private equity leaders, and cutting-edge fintech disruptors, this is where they meet to forge partnerships, spark dialogue, and shape the future of finance.

{kind=link}