Table of Contents

This piece serves as a springboard for brn's exploration of the broader macroeconomic landscape. As your trusted partner in navigating the digital asset space, brn goes beyond the realm of cryptocurrencies, recognizing the interconnectedness of traditional and digital markets.

- Dampened Rate Cut Expectations: The strong economic data has led investors to reassess the likelihood of substantial Fed rate cuts in 2024. This reduces the appeal of cryptocurrencies as a hedge against inflation, potentially leading to a sell-off in the near term.

- Risk-on/Risk-off Trade: While cryptocurrencies are not directly impacted by US interest rates, they are susceptible to broader risk sentiment. A shift away from risk-on assets due to the Fed's hawkish stance could trigger a decline in crypto prices.

- Bitcoin Halving Event: The upcoming Bitcoin halving, which reduces the number of new coins minted, remains a bullish factor for the long term. However, the short-term price action may be volatile due to the interplay of the Fed's monetary policy and broader market sentiment.

April got off to a bad start for stocks and cryptocurrencies after US factory data surprised everyone and expanded for the first time since 2022, with input costs climbing too, suggesting a revival in inflationary pressures.

Just before the data release, Bitcoin was trading at over $70,000 and is currently down over 5% to trade a touch under $67,000.

Thanks to a surge in output and an increase in new orders, the ISM manufacturing index shocked everyone by entering growth territory for the first time since late 2022.

Markets interpreted that as reducing the chances of meaningful Fed rate cuts; nevertheless, construction was far weaker, and many more employment figures are coming.

More importantly, signs of mounting inflationary pressures are on the rise.

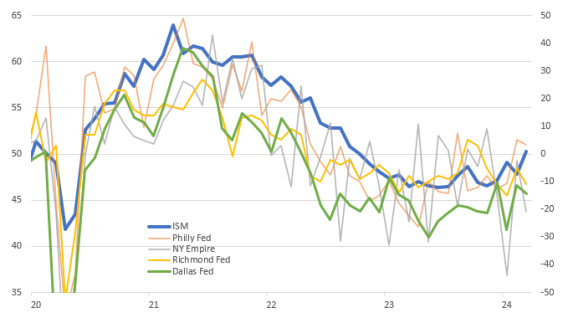

Unpredictable US ISM Readings Mirror China's

The February ISM manufacturing index has climbed above the break-even 50 threshold for the first time since September 2022.

Following an unexpected upturn in Chinese manufacturing PMIs over the weekend, the survey's entry into the growth zone provides optimism that the industrial sector is now stabilising after nearly 18 months of decline.

Since the regional surveys earlier showed declines, this may be the main explanation for the ISM's success (see chart below).

Despite the seeming concentration of effort to replicate the success of Asian surveys, no regional surveys have been conducted in the United States west of the Rocky Mountains.

The possibility of interest rate cuts has the markets wary.

There are about twenty separate speeches scheduled by the Fed this week, and the market is probably pricing in the possibility that policymakers may be hesitant to commit to substantial policy easing.

But, there are also many employment data releases during the week, building up to Friday's non-farm payrolls and unemployment rate.

As expected, the data-dependent Fed is not making much headway in this regard with the latest data.

It appears that comparing the data from the first quarter of 2024 with the data from the second half of 2023 shows that data is going in the opposite direction for prospective rate cuts.

Fed Chair Powell said he would wait for further evidence before changing the rate cut predictions for 2024.

Fed's June Rate Cut in Jeopardy

Bond dealers temporarily set the probability of a first move in June to less than 50% and priced in less monetary policy easing by the Fed this year than the dot plots show.

Following March's ISM manufacturing report that blew away all expectations, the amount of Fed easing factored into swap contracts for this year fell to less than 65 basis points, less than what Fed policymakers had predicted.

As a result, bond prices fell and yields on government bonds with maturities across the curve - ranging from two to thirty years - increased by 10 basis points, the largest daily gain this year.

Selling Pressure Across Assets

Cryptocurrencies and global stocks join losses in the world’s biggest bond market after strong US economic prospects and pushback in rate cut expectations.

Global stocks dropped after the S&P 500 marked its fifth month of gains.

Following a fantastic quarter for equities, investors are putting their money on the idea that the Fed can pull off a soft landing, which is why the data is so surprising. With a 10% gain in Q1, the benchmark S&P 500 has set a new record 22 times this year, increasing the value of US equities by $4 trillion.

Still, the S&P 500 is up over 50% since the low point in October 2022 and when compared to the low in March 2020, the US benchmark is up over 140%. It's worth noting that it took around 5 years, from September 2002 to July 2007, for the S&P 500 to increase by 110%.

But regardless of the direction of equities, investors are preparing for what lies ahead after taking profits from the S&P 500's impressive first quarter performance.

As we move into the second quarter, the stock market is currently at an unprecedented high. However, the options market is providing valuable insights into traders' sentiments.

There has been a minimal interest in put options that generate profits from minor corrections for quite some time.

Traders, on the other hand, are discreetly acquiring tail-risk hedges, which offer safeguards against significant stock market fluctuations but do not address the impact of minor downturns.

The surge in the S&P 500 has led to increased valuations across the market, as evidenced by the equal-weighted version of the benchmark index.

In this version, companies such as Nvidia hold the same significance as Dollar Tree, resulting in a valuation that exceeds 17 times earnings.

Some are concerned that the market is getting too heated due to the quick rise.

Crypto in Buy/Sell the News Mode

While crypto isn't very affected by US Risk-Free rates, a general risk-on/risk-off attitude does have a significant second-order influence, suggesting a sell or buy the news before the halving event.

With the halving cycle, ETF flows surpassing all prior ETFs and predictions, and the fact that we have broken above BTC's (and TradFi's) all-time highs, there are solid reasons to be long the largest crypto.

If there isn't a significant breakthrough leading to new all-time highs in BTC, those who have invested in long call volatility may not see a substantial return on their investment.

The current positioning is quite stretched, potentially resulting in an intriguing "sell-the-news" halving cycle play in the market.

In the event of a substantial market downturn, many open interest positions could be closed.

This could change the volatility skew, with a greater emphasis on put options and a decrease in the price difference between related financial instruments.

The market is favouring long positions leading up to the halving, although it remains challenging to make accurate predictions due to the high level of participation from all parties.

Investment Implications

Investors should be cautious in the near term as crypto markets adjust to the revised expectations for Fed policy. While the Bitcoin halving event offers long-term upside potential, the possibility of a "sell-the-news" scenario surrounding the halving cannot be ruled out.

Investors with a short-term horizon may want to consider hedging their exposure or adopting a wait-and-see approach.

{kind=link}